Evaluating Cybersecurity Preparedness at Asset Managers – Part One

Here, we evaluate cybersecurity preparedness, highlighting some of the key prevention measures we look for in asset managers in today’s environment.

Past performance is not necessarily indicative of future results. No assurance can be given that any investment will achieve its given objectives or avoid losses. Unless apparent from context, all statements herein represent GCM Grosvenor’s opinion.

Social distancing and remote workforces are the new normal. Many organizations around the world are managing their businesses, personnel, and client relationships without the benefit of in-office staffs. As companies consider how and when to re-open, it’s increasingly apparent that the return to entirely onsite workforces won’t happen any time soon, if ever.

Against this backdrop, asset managers and investors are evaluating the risks associated with performing diligence on managers, funds, and investments without the benefit of site visits or in-person meetings. These firms must in turn reassure their clients that they can still conduct a robust research process remotely.

In the following, we explore some of the challenges – and unforeseen benefits – of performing remote due diligence, and discuss what we believe makes a well-resourced, sophisticated investor properly positioned to conduct due diligence in this environment.

There are legitimate concerns among investors and their clients about the effect of social distancing on the due diligence process. Many investors fear that without the opportunity to meet a manager face-to-face, watch their body language, assess their culture, and tour their offices, the evaluation of that manager may be incomplete, and thus presents risks.

However, some interesting benefits of the new normal have emerged. Video meetings are easier to schedule and attend; they can be shorter and more frequent, are canceled less often, and more attendees can be in the “room.” Meanwhile, limited travel has created cost savings for both investors and managers (particularly benefiting emerging managers), and senior staff members are generally more available for these calls.

This backdrop has created a scenario in which investors that are better equipped to navigate the potential challenges may harness the potential benefits of conducting due diligence in the current environment. Here, we describe the particular traits of these well-positioned investors.

We believe that a well-prepared investor will be able to mitigate the challenges of a remote work environment and successfully capitalize on its advantages. We’ve identified some key characteristics of such investors:

Investors that maintained robust rosters of managers before the COVID-19 crisis are well-positioned for today’s challenging environment. These investors can more easily capitalize on a quickly changing investment landscape by leveraging their manager relationships to efficiently evaluate deals and sponsors. Or, those seeking to invest with a manager that they know but have not yet invested capital can more successfully perform due diligence and allocate capital remotely because of their familiarity with the manager in question. For investors without these relationships, it can be difficult to confidently execute full due diligence on unfamiliar managers through virtual-only interactions. This applies to both established and small and emerging managers.

It is critical that an investor’s roster includes small and emerging managers, complete with a database of critical information such as performance track records, as these managers can identify opportunistic investments and strategies that may not be captured by larger managers. Often, smaller managers are spin-offs from established firms, which again stresses the importance of a wide network of relationships. Investors with broad relationships, robust monitoring, and multiple touch-points at large firms will be more familiar with portfolio managers, and therefore they have a first-mover advantage when those portfolio managers launch their own firms.

The current environment should not have a seismic impact on investors who have long been supplementing in-person investment due diligence meetings with a host of research activities and analytics. These investors already use remote technology, log countless hours on audio and video conferences with managers around the world, and use digital solutions to exchange sensitive data and reports. They also have robust screening mechanisms and monitoring platforms and are highly adept at performing reference checks.

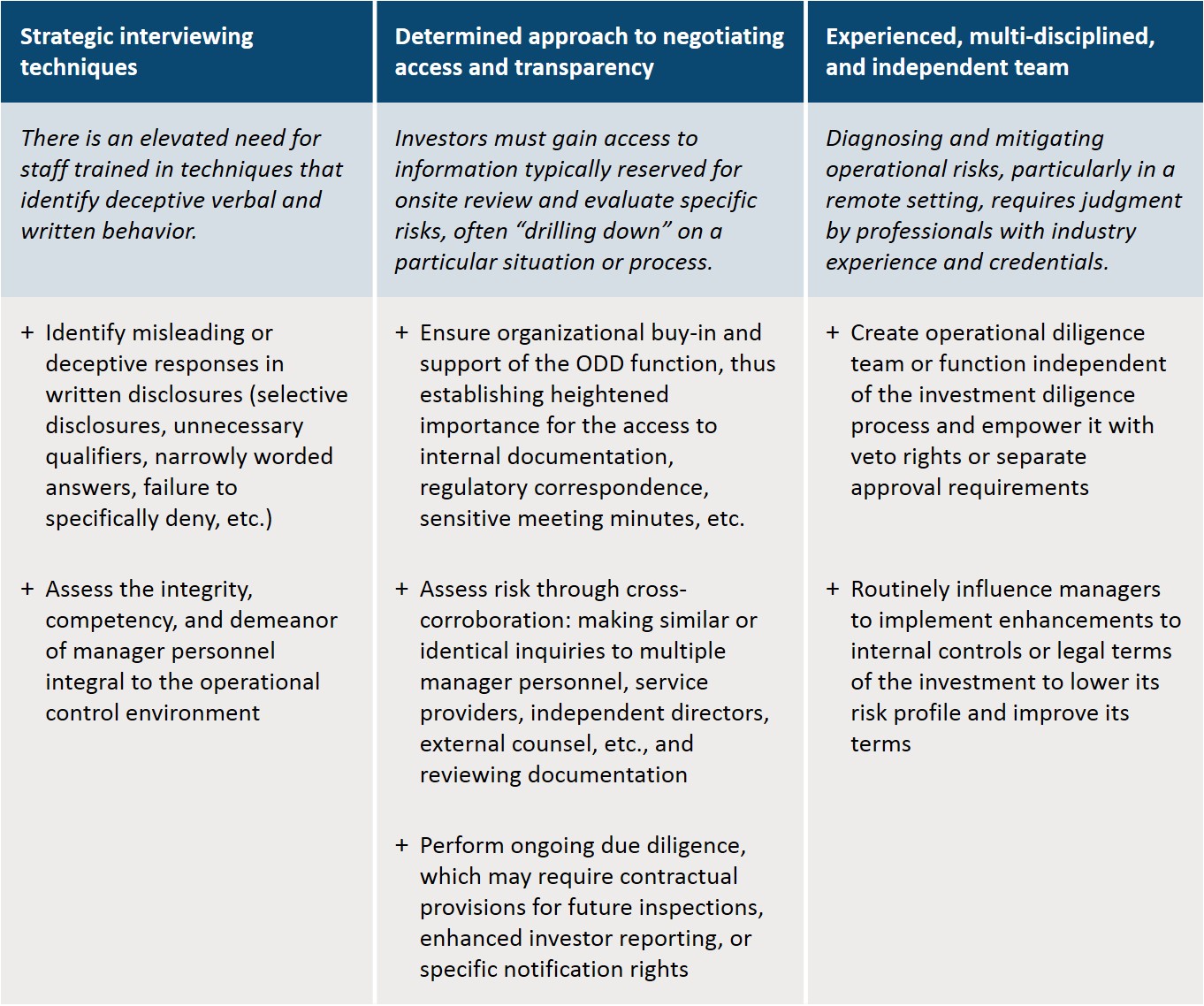

From an operational perspective, we believe that social distancing restrictions have highlighted the importance of a robust operational due diligence (ODD) program. Among the key objectives of ODD is to confirm and corroborate a manager’s investment operations and internal control environment by evaluating its operational systems, processes, and team. But certain aspects of these confirmation procedures may be challenging when in-person meetings or site visits are not allowed.

Therefore, a full ODD “toolkit” is critical to thoroughly evaluate managers from an operational risk perspective, in a remote setting. This toolkit includes, but is not limited to, extensive experience performing background checks, strategic interviewing techniques, strong negotiation skills, competence in making detailed reference calls with key service providers, and various technology solutions to mimic the in-person experience. While these activities can be completed remotely, without applying the full toolkit and ample resources, there is potential for increased risk. (See “A closer look” below for more.)

While the above due diligence activities are rigorous and extensive, we believe they must also be flexible and adaptive, particularly in today’s environment. For example, refusing to acknowledge or permit comprehensive remote due diligence as a suitable alternative for in-person or onsite visits(s) may unnecessarily delay or prohibit an investment. Instead, flexible investors will think differently about what constitutes an “onsite” visit and how to achieve its objectives within an overall due diligence process remotely.

Specific to the ODD process, virtual tours, pre-prepared videos, office floorplans, electronic access to sensitive information, system demos, or other activities may together suffice, assuming the ODD professionals are experienced and prepared to thoroughly evaluate the results of these alternate procedures. In these cases, an investor must have the confidence to move forward with an investment (or reject it) based on the entirety of the due diligence (investment, risk, and operational) completed, inclusive of the supplemental remote work performed.

Finally, we believe large investors with sizable amounts of capital in the market and strong reputations will benefit in the current situation. Managers are more apt to give these investors time, attention, and access because of their position in the market and familiar name. While this is a common view in any environment, today it is a different side of the same coin – in an environment of heightened risk and uncertainty, managers that cannot meet investors face-to-face may take comfort in knowing they chose a high-quality partner.

Despite the potential challenges presented by the current environment, we believe that we are well-suited to flexibly adapt and, potentially, capitalize on the opportunities presented. Our $55 billion global investment platform and robust roster of more than 600 manager relationships allow us to quickly and effectively identify and capitalize on opportunities on behalf of our clients. We believe our size and scale combined with our 50-year history, established track record, and institutional client base position us well to effectively deploy capital in the current environment.

Remote due diligence procedures have been integral to our overall due diligence efforts for years, so this new normal is not so new to us. Our Investment Committee has reviewed and confidently approved many investments without the investment team going on site.

In addition, our operational due diligence toolkit is comprehensive. We have an independent and experienced team of 15 professionals whose primary focus is performing ODD. The team is trained by former CIA, FBI, and law enforcement professionals in strategic interview techniques and behavioral assessment tactics. We evaluate investment opportunities on a case-by-case basis since each presents a unique set of considerations – including whether to incorporate a site visit into the process. In the current environment, we continue to perform a tailored risk assessment to thoroughly evaluate operational risk.

While we believe that remote due diligence will be sufficient in many cases, should a material issue arise during our due diligence process that we cannot fully diligence or sufficiently mitigate, we would not invest. Said another way, our due diligence underwriting standards and views towards investment and operational risk remain the same regardless of how or where we perform the work.

Finally, we have an extensive roster of, and over $19 billion invested with, small and emerging managers who represent an important source of differentiated deal flow that we may access quickly. We continue to keep the emerging manager industry connected and build relationships with this community – even virtually – by participating in and hosting conferences such as the recent Consortium, which brought together over 500 managers, LPs, and consultants in a virtual setting.

While the current environment has many challenges, we believe that we have adapted a nimble approach that will allow us to continue our investment activities on behalf of our clients.

Here, we evaluate cybersecurity preparedness, highlighting some of the key prevention measures we look for in asset managers in today’s environment.

We explore some challenges and unforeseen benefits of performing remote due diligence, and discuss what we believe makes a well-resourced, sophisticated investor properly positioned to conduct due diligence in this environment.

Important Disclosures

For illustrative and discussion purposes only.

No assurance can be given that any investment will achieve its objectives or avoid losses. Past performance is not necessarily indicative of future results.

The information and opinions expressed are as of the date set forth therein and may not be updated to reflect new information.

Investments in alternatives are speculative and involve substantial risk, including strategy risks, manager risks, market risks, and structural/operational risks, and may result in the possible loss of your entire investment. The views expressed are for informational purposes only and are not intended to serve as a forecast, a guarantee of future results, investment recommendations, or an offer to buy or sell securities by GCM Grosvenor. All expressions of opinion are subject to change without notice in reaction to shifting market, economic, or political conditions. The investment strategies mentioned are not personalized to your financial circumstances or investment objectives, and differences in account size, the timing of transactions, and market conditions prevailing at the time of investment may lead to different results.

GCM Grosvenor®, Grosvenor®, Grosvenor Capital Management®, GCM Customized Fund Investment Group®, and Customized Fund Investment Group® are trademarks of Grosvenor Capital Management, L.P. and its affiliated entities. This document has been prepared by Grosvenor Capital Management, L.P., GCM Customized Fund Investment Group, L.P., and GRV Securities LLC. ©2020 Grosvenor Capital Management, L.P., GCM Customized Fund Investment Group, L.P., and GRV Securities LLC. All rights reserved. Grosvenor Capital Management, L.P. is a member of the National Futures Association.

GCM Investments UK LLP (“GCMUK”) has been made aware of fraudulent schemes targeting members of the public in Spain.

Unauthorised individuals are falsely claiming to represent GCMUK and are misusing the firm’s name and publicly available information in connection with fake investment opportunities.

These scams are sophisticated and deliberately misleading. They may involve the use of real GCMUK employee names and may imitate the tone, format, and branding of genuine GCMUK communications.

Please note:

GCMUK does not offer financial services or investment products to retail clients, either directly or through third parties. You can verify GCMUK’s regulatory status and permissions on the UK Financial Conduct Authority (FCA) Register at register.fca.org.uk

If you are based in Spain and believe you have been contacted by a fraudster claiming to represent GCMUK, please take the following steps:

You may also report online fraud to the Spanish National Police or Civil Guard via the computer crime reporting service at www.policia.es.

GCM Investments UK LLP (“GCMUK”) ha tenido conocimiento de estafas dirigidas al público en España.

Personas no autorizadas afirman falsamente representar a GCMUK y están haciendo un uso indebido del nombre de la empresa y de la información disponible públicamente en relación con oportunidades de inversión falsas.

Estas estafas son sofisticadas y deliberadamente engañosas. Pueden implicar el uso de nombres reales de empleados de GCMUK e imitar el tono, el formato y la marca de las comunicaciones auténticas de GCMUK.

Tenga en cuenta lo siguiente:

GCMUK no ofrece servicios financieros ni productos de inversión a clientes minoristas, ni directamente ni a través de terceros. Puede verificar el estado regulatorio y los permisos de GCMUK en el Registro de la Autoridad de Conducta Financiera del Reino Unido (FCA) en register.fca.org.uk

Si reside en España y cree que ha sido contactado por un estafador que dice representar a GCMUK, siga los siguientes pasos:

También puede denunciar el fraude online a la Policía Nacional o la Guardia Civil española a través del servicio de denuncia de delitos informáticos en www.policia.es.

GCM Investments UK LLP (“GCMUK”) has been made aware of fraudulent schemes targeting members of the public in France.

Unauthorised individuals are falsely claiming to represent GCMUK and are misusing the firm’s name and publicly available information in connection with fake investment opportunities.

These scams are sophisticated and deliberately misleading. They may involve the use of real GCMUK employee names and may imitate the tone, format, and branding of genuine GCMUK communications.

Please note:

GCMUK does not offer financial services or investment products to retail clients, either directly or through third parties. You can verify GCMUK’s regulatory status and permissions on the UK Financial Conduct Authority (FCA) Register at register.fca.org.uk.

If you are based in France and believe you have been contacted by a fraudster claiming to represent GCMUK, please take the following steps:

You may also report online scams through the French government’s Pharos platform at www.internet-signalement.gouv.fr.

GCM Investments UK LLP (“GCMUK”) a été informée de l’existence de stratagèmes frauduleux visant le grand public en France.

Des personnes non autorisées prétendent faussement représenter GCMUK et utilisent abusivement le nom de la société et des informations accessibles au public dans le cadre de fausses opportunités d’investissement.

Ces escroqueries sont sophistiquées et délibérément trompeuses. Elles peuvent impliquer l’utilisation des noms réels d’employés de GCMUK et imiter le ton, le format et l’image de marque des communications authentiques de GCMUK.

Remarque:

GCMUK n’offre pas de services financiers ni de produits d’investissement à des clients particuliers, que ce soit directement ou par l’intermédiaire de tiers. Vous pouvez vérifier le statut réglementaire et les autorisations de GCMUK dans le registre de la Financial Conduct Authority (FCA) du Royaume-Uni à l’adresse register.fca.org.uk.

Si vous êtes basé en France et pensez avoir été contacté par un fraudeur prétendant représenter GCMUK, veuillez suivre les étapes suivantes :

Vous pouvez également signaler les escroqueries en ligne via la plateforme Pharos du gouvernement français à l’adresse www.internet-signalement.gouv.fr.

ご注意

・当社代表取締役の駒田智彦(もしくはその秘書を名乗るもの)が、LINE等のSNSやメール等を通じて金融商品への投資をご案内・勧誘することはございません。

・不審なメールのリンク先には絶対にアクセスしないようご注意ください。

・GCM Grosvenorの日本法人であるGCMインベストメンツ株式会社は、Webページを開設しておりません。また、Instagram、LineといったSNSにおいても公式ページは開設しておりません。

GCM Investments UK LLP (GCMUK) has been made aware of fraudulent schemes targeting members of the public in the United Kingdom.

Unauthorised individuals are falsely claiming to represent GCMUK and are misusing the firm’s name and publicly available information in connection with fake investment opportunities.

These scams are sophisticated and deliberately misleading. They may involve the use of real GCMUK employee names and may imitate the tone, format, and branding of genuine GCMUK communications.

Please note:

GCMUK does not offer financial services or products to retail clients, either directly or through third parties. You can verify GCMUK’s regulatory status and permissions on the Financial Conduct Authority (FCA) Register at register.fca.org.uk.

If you are based in the UK and believe you have been contacted by a fraudster claiming to represent GCMUK, please take the following steps:

Investor Scam Alert

Unauthorized individuals are impersonating Winston Chow in scams targeting investors, particularly in Malaysia. He does not solicit investments directly in Asia. If you are contacted by someone claiming to be him outside of official channels, please report it to local authorities.

For verification or further information, please contact: [email protected]

Investor Scam Alert

GCM Grosvenor L.P. and its affiliated entities (collectively, “GCMG”) have been made aware of fraudulent schemes currently targeting members of the public in Malaysia and Hong Kong, in which unauthorised individuals are falsely claiming to represent GCMG in connection with purported investment opportunities.

These fraudulent individuals are believed to be actively promoting false investment opportunities, often involving mobile applications, through the unauthorised use of GCMG’s name, brand, corporate logo, and other identifying materials. We have also received reports that these parties may be distributing fabricated business cards, hosting online webinars, creating WhatsApp groups, and arranging personal video calls to simulate legitimacy. These scams are sophisticated and deliberately misleading, frequently involving the use of real GCMG employee names and imitating the style, tone, and presentation of genuine GCMG communications.

GCMG has no presence, operations, or authorised representatives in Malaysia. GCMG does not offer any investment schemes, products, or mobile applications targeted at Malaysian investors, either directly or indirectly.

While GCMG maintains a legitimate presence and employs personnel in Hong Kong, these scams are entirely unauthorised and unrelated to any genuine activities conducted by GCMG or its employees in the region.

Position of GCMG

GCMG has neither authorised nor endorsed any such solicitations and takes this matter seriously. We have reported some of these incidents to the relevant regulatory and enforcement authorities in Malaysia, and are doing the same in Hong Kong, including notifying the Hong Kong Police and the appropriate financial regulators. GCMG will continue to assist with their investigations.

GCMG is actively monitoring these developments and reserves all rights to take legal action against any party found misusing its name, brand, or intellectual property.

While these reports currently centre on activity in Malaysia and Hong Kong, the methods used may be replicated in other jurisdictions. GCMG continues to monitor for similar risks globally.

Unauthorized individuals are impersonating Winston Chow in scams targeting investors, particularly in Malaysia. He does not solicit investments directly in Asia. If you are contacted by someone claiming to be him outside of official channels, please report it to local authorities.

For verification or further information, please contact: [email protected]

We offer clients a broad range of tailored solutions across strategies, including multi-strategy, macro, relative value, long/short equity, quantitative strategies, and opportunistic credit. Levaraging our large scale and presence in the industry, we are able to offer clients preferntial exposure to hard-to-access managers and seek to obtain terms that can drive economic and structural advantages.