As investors look ahead to 2026, markets are being shaped by a combination of forces. Inflation remains persistent, fiscal dynamics continue to evolve, technological change is accelerating, and geopolitical uncertainty remains constant.

This environment places a premium on active management, flexible portfolio construction, and broad access across alternative strategies. At the firm’s 2026 Annual Forum, Chief Investment Officer Fred Pollock shared how GCM Grosvenor is approaching the year ahead and where he sees opportunity emerging amid complexity.

1. Uncertainty Is the Starting Point for 2026

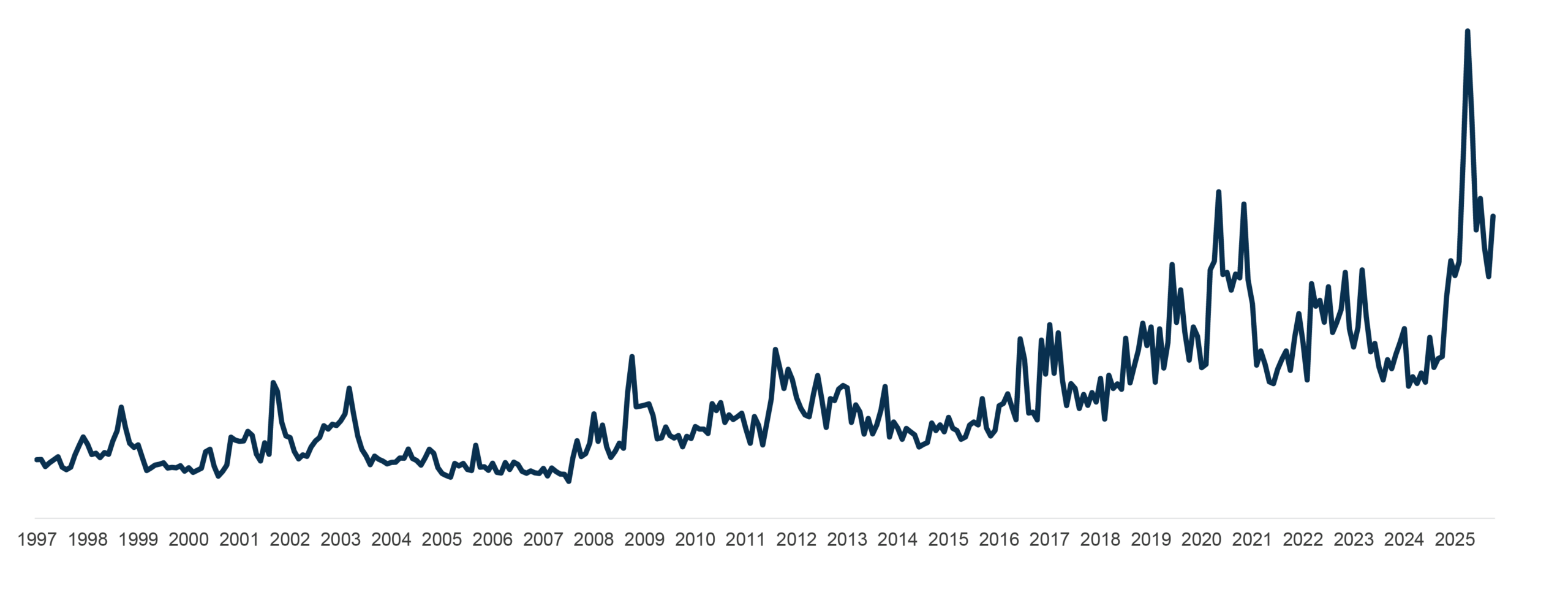

Economic, geopolitical, and policy uncertainty remain elevated entering the year. Inflation is still above target in many regions, financial conditions are tighter than in recent years, global trade is more fragmented, and geopolitical tensions continue to overlap.

What stands out is how markets have adapted. As Pollock noted, “markets can look one way early in the year and very different by year-end. Investors aren’t surprised by volatility anymore, which means you have to be more selective in how capital is allocated.”

For investors, this normalization of volatility reinforces the importance of selectivity and flexibility. Rather than stepping away from risk, success in 2026 is more likely to come from understanding where risk is being compensated in the form of returns and where it is not.

FIGURE 1: GLOBAL ECONOMIC POLICY INDEX

Data as of December 31, 2025.

Data Source: Bloomberg Finance, L.P.

Link to explanation of the policy uncertainty index: Economic Policy Uncertainty Index

2. Fiscal Constraints Increase the Importance of Portfolio Construction

A defining feature of the current environment is the growing strain on government balance sheets across developed markets. Large and persistent deficits in the U.S., Europe, and Japan, driven by aging populations, political pressures, higher interest costs, defense spending, and energy transition investments, continue to push sovereign debt higher relative to growth.

As governments rely more heavily on market refinancing, increased bond supply has contributed to rising yields. While this may limit the scope for policy intervention in future downturns, it also places greater responsibility on investors to rely on portfolio construction, manager selection, and diversification as drivers of outcomes.

As Pollock cautioned, coordination between governments and central banks may be more limited in the next period of market stress. In that context, resilient portfolio design becomes even more important.

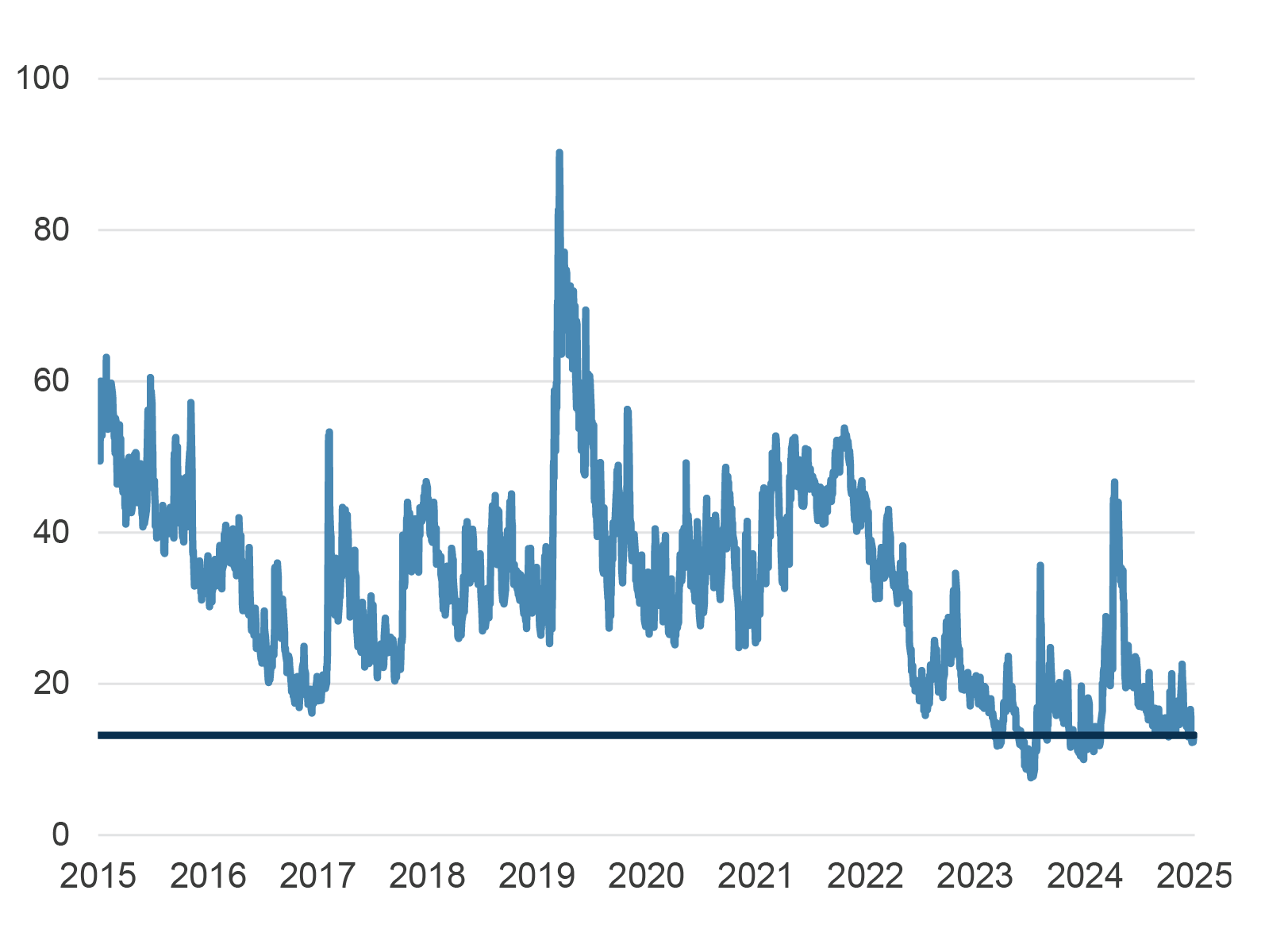

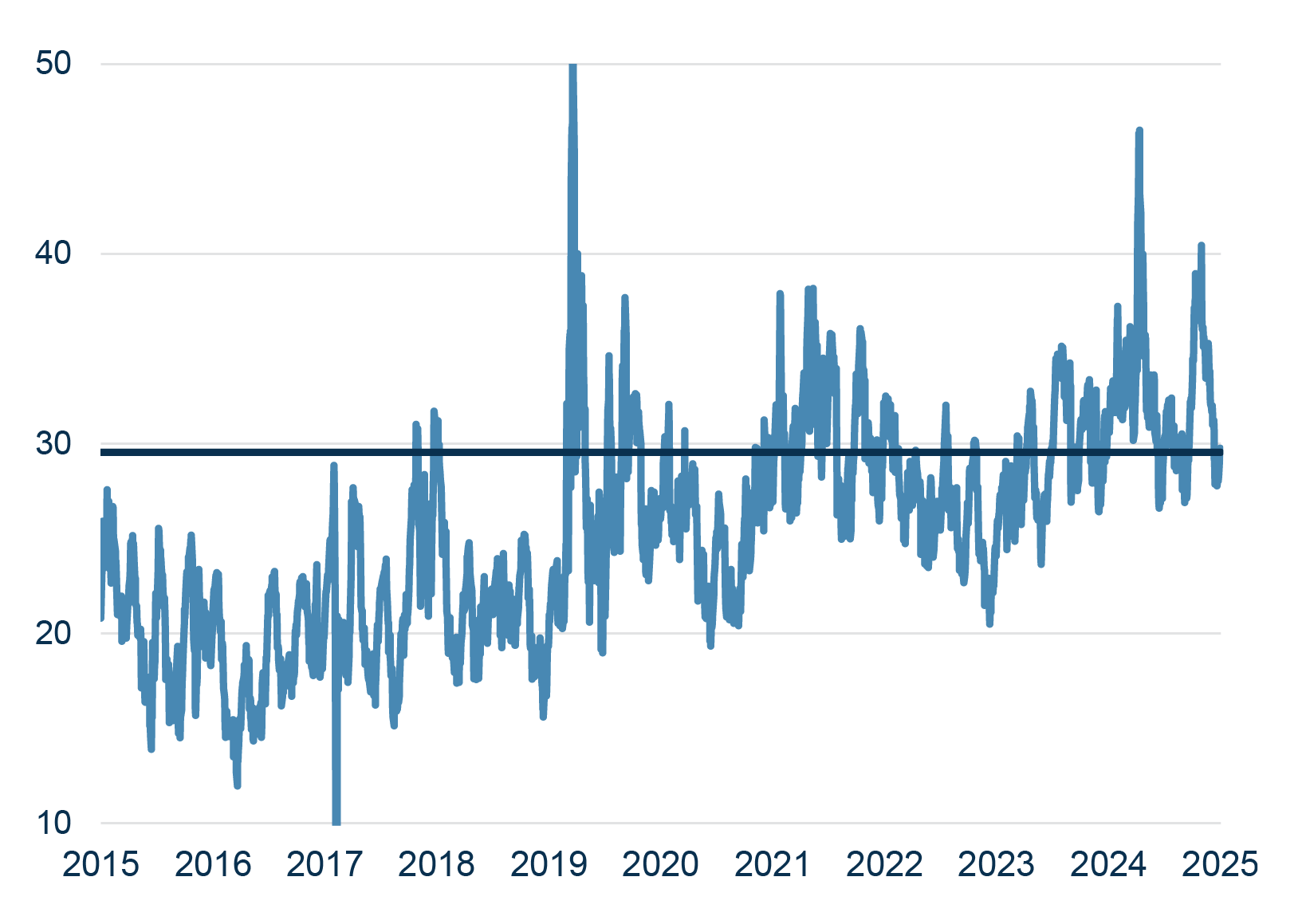

FIGURE 2: Dispersion & Correlation

Low Correlations Facilitate Portfolio Diversification

CBOE 3 month Implied S&P 500 Correlation Index

High levels of dispersion can provide alpha opportunity

CBOE S&P 500 Dispersion Index

Data as of December 31, 2025.

Data Source: Bloomberg Finance, L.P.

Past performance is not necessarily indicative of future results. No assurance can be given that any investment will achieve its objectives or avoid losses.

3. Elevated Valuations Change the Source of Returns

Valuations remain elevated across many markets, particularly in U.S. equities, reflecting optimism around AI-driven growth. Credit markets show a similar dynamic, with spreads compressed despite higher policy rates.

Together, these conditions suggest that broad market returns may be more modest, while differences at the security and sector level become more pronounced. As Pollock noted, "high valuations don’t mean you stay out of markets. They do change how you invest.”

In this environment, returns are likely to be driven less by market exposure and more by careful selection, disciplined underwriting, and thoughtful implementation.

4. Private Markets Reward Discipline and Access

Private equity enters 2026 following several years of adjustment. Valuations have moderated, liquidity has declined, transaction activity remains below prior peaks, and alternative liquidity solutions such as continuation vehicles and single-asset secondaries have become more common.

Fundraising has become increasingly bifurcated, with high-performing managers continuing to raise capital efficiently while others face greater challenges. While this environment can be difficult, it also creates opportunity for allocators with strong relationships and disciplined pacing.

Looking ahead, a more active IPO market, particularly for late-stage growth companies, could help improve liquidity in select areas. Even so, outcomes are likely to depend more on portfolio construction than on market timing.

5. Infrastructure, Absolute Return Strategies, Real Estate, and Credit Support Portfolio Resilience

Infrastructure continues to benefit from supportive long-term fundamentals as demand across energy, digital, and essential services drives a growing opportunity set. The asset class has been a clear beneficiary of sustained capital demand, and investor appetite remains strong. At the same time, significant capital flows into AI-related infrastructure underscore the importance of careful underwriting, particularly when assessing long-term assumptions around residual values and power market dynamics. In this environment, disciplined region- and subsector-level differentiation is critical.

In a market environment characterized by faster change, absolute return strategies are also well positioned. Elevated dispersion, lower correlations, and shifting fundamentals across sectors and regions expand the opportunity set for managers focused on security selection and risk management. Investor interest has strengthened as the zero-rate period recedes, and the value of liquidity, downside mitigation, and uncorrelated returns becomes more apparent.

In real estate, value creation increasingly depends on structuring and execution. Approaches such as joint ventures, seeding arrangements, and alignment with operating partners are becoming more important as investors seek to enhance risk-adjusted returns. With capital having stepped back from certain areas of the market, the coming years may present attractive entry points for investors with dry powder and a selective approach.

Within credit, portfolio construction continues to evolve toward broader diversification across sub-asset classes, managers, and implementation types. Investors are increasingly combining primary investments with secondaries and co-investments to build more flexible and resilient credit exposures that can adapt as market conditions change.

Looking Ahead

The outlook for 2026 is complex, but not pessimistic. While uncertainty, elevated valuations, and fiscal constraints raise the bar, they also create an environment where thoughtful strategy and execution matter more.

At GCM Grosvenor, the year ahead is approached with confidence. The firm’s open-architecture platform, emphasis on customization, and ability to remain active across public and private markets are well suited to the conditions investors face today.

As Pollock emphasized, “A sit-it-out strategy won’t work in this environment. Investors need to remain agile and prepared to move quickly as markets evolve.” For investors, the challenge in 2026 is not prediction, but preparation.