As the GP-led continuation vehicle market surpasses $100 billion in annual volume for the first time, it has cemented itself as a permanent feature—a de facto fourth exit option—in the private equity landscape. Investors are increasingly focused on the skills, relationships, and strategies required to generate differentiated performance in this rapidly maturing segment.

Many secondary players seek to differentiate themselves by emphasizing the importance of being a “lead investor,” or in the case of direct private equity shops, their underwriting and sector expertise. While these capabilities may offer advantages, we believe the most compelling advantage lies elsewhere: being an existing investor in the selling fund, having an established relationship with the sponsor, and investing at a size that allows participation in a broader range of deals as a syndicate member.

This article outlines three interrelated dynamics shaping the GP-led continuation vehicle market today: the structural role of syndication, the role of the lead investor, and the expanding participation of an increasingly diverse and growing universe of investors.

State of The GP-Led Continuation Vehicle Market

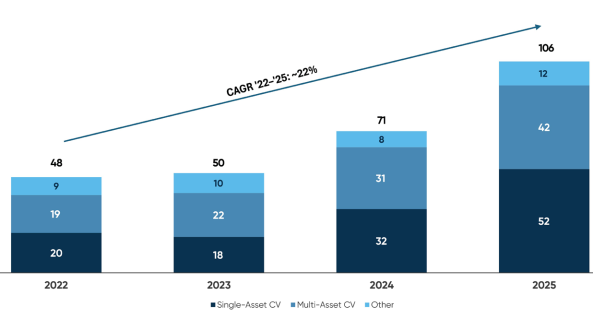

The continuation vehicle (CV) market reached a record $106 billion in closed transaction volume in 2025, a year-over-year increase of approximately 51%.1 This growth reflects a structural shift in how private equity sponsors manage their portfolios, rather than a cyclical response to constrained exit markets. CVs are now mainstream: 83% of the top 100 global buyout sponsors have accessed the continuation vehicle market since inception, and 58% of CV volume originated from repeat sponsor issuers in 2025.2 Continuation vehicles represent approximately 15% of total sponsor-backed exit value, up from 8% in 2021.3

The buy-side universe has expanded in parallel. Participation continues to expand as traditional buyout sponsors launch dedicated GP-led strategies and established secondary buyers raise specialized GP-focused funds. Eight of the largest direct private equity firms now have secondaries capabilities. This institutionalization of the buy-side has introduced more capital, more competition, and a wider range of claimed sources of competitive differentiation.

SPLIT BY DEAL TYPE ($BN OF TRANSACTION VOLUME)

SOURCE: Evercore PCA, 2025 Secondary Market Report, February 2026.

Why Syndication Matters

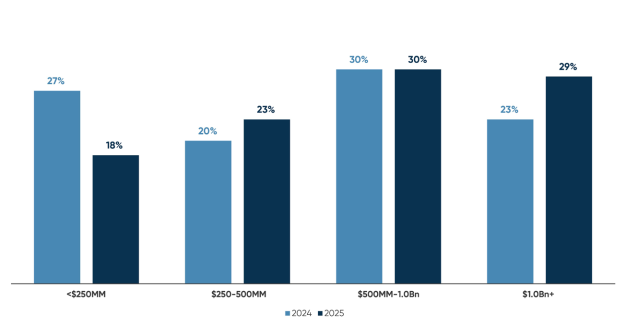

One of the clearest features of the current market is scale, with important implications for how transactions are executed. The average continuation vehicle transaction size increased more than 15% year-over-year to approximately $1 billion in 2025, and the number of $1 billion-plus CVs increased 57% compared to 2024.4 Meanwhile, the average LP rollover rate in CV transactions was approximately 15%.5 This low rollover rate,combined with increasingly large transaction sizes, creates a significant gap that must be filled by new secondary capital.

Even in small- and mid-sized transactions—where GCM Grosvenor is most active—syndication plays a central role in transaction execution. Evercore found that continuation funds with capital raises between $250mm and$500mm involved an average of 7 new investors, while those between $500mm and $1bn involved 12 investors. At the upper end of the market, transactions above $1bn averaged 17 participants.6 In each case, the lead investor anchors the process, but a meaningful share—and sometimes the majority—of capital formation depends on a broader syndicate.

CONTINUATION FUND TRANSACTION SIZE

SOURCE: Morgan Stanley, FY 2025 Continuation Fund Market Review, February 2026.

The Lead Investor Role

In most continuation vehicle transactions, a single investor (or occasionally a small group of co-leads)assumes the lead role: leading diligence, setting price, and negotiating terms and governance. Importantly, however, the sponsor—not the lead investor—ultimately determines which investors receive an allocation to the deal. Having a strong relationship with the sponsor, or being viewed as a potential long-term partner, can be critical.

The lead investor role matters in transactions that are likely to be oversubscribed, as lead investors are often guaranteed a baseline allocation in the deal. However, GCM Grosvenor finds that being an existing investor in the sponsor’s funds is equally as instrumental in securing favorable allocations in oversubscribed deals. Sponsors increasingly reserve part of the CV for syndicate members, viewing the transaction as a relationship-building tool to reaffirm existing relationships as well as grow and diversify their future LP base. William Blair found that approximately 60% of secondary investors committed primary capital to a sponsor’s flagship fund following a continuation fund transaction in 2024.7 Even in cases where we do not have an existing investment with the sponsor, we are often considered a syndicate member of choice given our ability—but not obligation—to participate as a primary investor in the sponsor’s future funds. As a large existing LP—and frequently an LPAC member—in many of the funds pursuing CVs, GCM Grosvenor is typically aware of transactions before they go to market. This early visibility and the ability to register interest with the sponsor before a broader process is launched has historically helped secure allocations in competitive situations.

As the continuation vehicle market has matured, deal processes and economic terms have become increasingly standardized, making many of the advantages traditionally attributed to lead investors more broadly accessible across the buyer universe.

DUE DILIGENCE. In the vast majority of CV transactions, both lead and syndicate investors have access to comprehensive data rooms that include quality of earnings reports, third-party industry analyses, management presentations, valuation reports, financial projections, and other relevant documentation. Syndicate investors also typically have access to the sponsor and the portfolio company’s management team and can request detailed customized analyses from the sponsor.

Additionally, as an existing investor in many of the managers and funds that organize continuation vehicles, GCM Grosvenor has often followed the underlying asset for years and has deep familiarity with the manager’s investment approach and sector expertise. This accumulated knowledge provides a diligence advantage that is distinct from simply being the first to enter a data room.

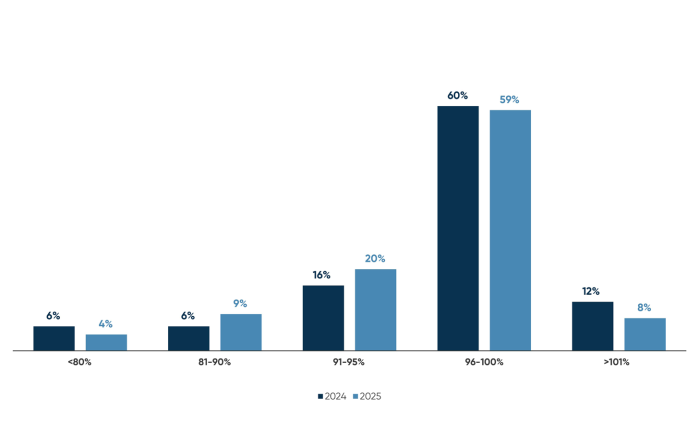

BUYOUT SINGLE ASSET CONTINUATION FUNDS WEIGHTED AVERAGE GP-LED PRICING OVER TIME

SOURCE: Morgan Stanley, FY 2025 Continuation Fund Market Review, February 2026.

PRICING. Continuation fund pricing has remained around par to a slight discount.8 The sponsor may not be incentivize to maximize value in a continuation vehicle process—rather they typically seek a fair balance that retains credibility with existing LPs while attracting new capital. The pricing dynamic in continuation vehicles is structurally different from a competitive auction—a dynamic that benefits all participants in the process, not just the lead.

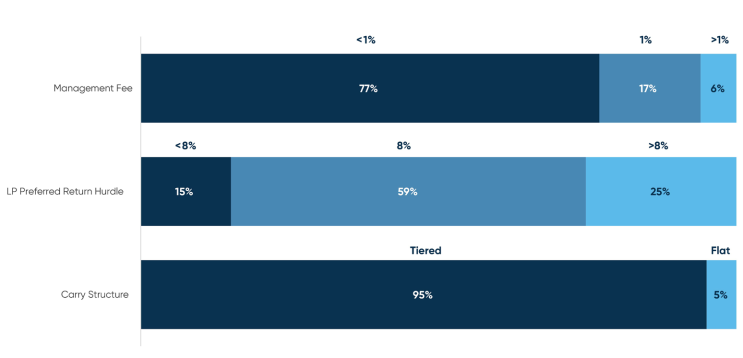

TERMS AND GOVERNANCE. Economic terms across the continuation vehicle market have converged around a relatively standardized framework, with the vast majority of CVs having a <1% management fee, 8%preferred return hurdle, and tiered carry structure.9

CV KEY TERMS (% OF VOL.)

SOURCE: Greenhill, FY 2025 Global Secondary Market Review, February 2026.

Preferential terms for lead investors are common—41% of continuation vehicle deals offered preferred terms for lead investors in 2025.10 However, these discounts are generally moderate and tend to be a function of larger check sizes rather than lead status. Moreover, any fee savings at the deal level should be weighed against the higher management fees and carried interest typically charged by many dedicated GP-led funds relative to traditional secondary vehicles. On a net-of-fees basis, the economic difference narrows.

From a governance standpoint, incoming buyers in continuation vehicles acquire largely passive interests in a limited partnership. The lead role may confer greater process influence, and, in some cases, an LPAC seat, but the investment still exists within the framework of a limited partnership interest in a fund with no special operational control or board representation at the company level.

CROSS-FUND INVESTMENTS AND ALIGNMENT. In 2025, approximately 50% of CV transactions involved a cross-fund investment by the sponsor to support capitalization and enhance alignment.11 Some lead investors, particularly those with large funds and/or SMAs, may prefer reduced or no cross-fund participation—where the sponsor invests capital from its latest active fund alongside the continuation vehicle—as such investments reduce available capacity for incoming secondary investors. In smaller transactions, cross-fund investments limit the ability of leads to invest at scale. GCM Grosvenor views cross-fund participation favorably, as it demonstrates strong alignment between the sponsor and the continuation vehicle. Of the continuation vehicles GCM Grosvenor has invested in since January 2020, 61%have included cross-fund investments. continuation vehicle market have converged around a relatively standardized framework, with the vast majority of CVs having a <1% management fee, 8%preferred return hurdle, and tiered carry structure.12

Overall, syndicate investors invest at the same price and on largely the same terms as lead investors. Leading helps secure early access and early allocation but participating in the syndicate is often economically equivalent and strategically sensible—particularly for an investor like GCM Grosvenor with a relatively modest target investment size and strong, established sponsor relationships. We have also seen that in some processes, particularly those run competitively with room for only one lead investor, cover bidders may be excluded from participating in the syndicate—the banker encourages each lead candidate to submit a best-and-final bid, and the losing bidders may be excluded from the deal entirely.

Asset-Based vs. Sponsor-Based Strategy

As the GP-led market has matured, a growing number of traditional buyout sponsors have launched dedicated continuation vehicle strategies—including Leonard Green, H.I.G. Capital, HgCapital, Warburg Pincus, and New Mountain—leveraging their existing investment platforms. These “direct-style” CV investors emphasize an “asset-based” approach to the CV market—one built on proprietary deal flow from their platforms, a more rigorous bottom-up underwriting, and the ability to add operational value post-close. How these capabilities translate to the continuation vehicle market, however, is less straightforward.

NARROWER OPPORTUNITY SET. The universe of deals available to direct-style CV investors may be narrower than it appears. Sponsors may not want direct private equity shops participating in their GP-led transactions for competitive and confidentiality reasons—for example, the risk that the buyer’s buyout team might compete against the sponsor for a future acquisition, use diligence information to inform a competing bid, or seek to exert operational influence that conflicts with the sponsor’s own value creation plan.

Sponsors generally prefer buyers who are existing investors in their funds or who can make future primary commitments. They view CV syndicate selection as a strategic opportunity to deepen relationships with or broaden their LP base. For direct-style investors who lack primary market scale, this preference can further limit the universe of accessible deals.

One consequence of this dynamic is that these direct-style investors may compete for deals by offering a higher purchase price or premium economic terms. In 2025, Morgan Stanley reported a notable uptick in “super carry”—carried interest tiers greater than 20%—in single-asset continuation vehicle transactions.13 This dynamic has coincided with the growth of traditional buyout sponsors entering the GP-led market.

UNDERWRITING AND SECTOR EXPERTISE. Continuation vehicles are not buyouts. The existing sponsor remains the control owner, has typically owned the company and worked with the management team for years, and is selecting an asset it believes can support another period of value creation. As a secondary investor in a CV, the critical underwriting questions extend beyond whether the asset is attractive to include fairness of the valuation, the alignment of interests, the quality of the sponsor, the structural terms of the new vehicle, and the go-forward economics.

Direct-style investors may bring sector expertise, but whether it is additive in a continuation vehicle is less clear. There is arguably no participant in the process—lead investor, syndicate member, or otherwise—who knows the asset, its management team, and its competitive dynamics better than the sponsor who has controlled it. A secondary investor’s role is to partner with that sponsor. For these reasons, GCM Grosvenor’s underwriting process places significant emphasis on the quality and track record of the sponsor itself—the sponsor’s history of value creation in the relevant sector, the depth of the operating team, and the credibility of the go-forward plan. GCM Grosvenor was an investor with the underlying sponsor in 76% of the CV deals it has invested in since January 2020.14

Further, the claim of more robust bottom-up underwriting by direct private equity firms may not be as differentiated as it appears. As previously discussed, most CVs offer transparent and comprehensive data rooms and access to management teams. Many sponsors also conduct a complete re-underwrite of the company and the market and bring the deal to their respective investment committees, particularly when a cross-fund investment is made. In our experience, direct private equity firms have demonstrated limited unique diligence requirements or company-specific insights in connection with GP-led processes, although we have seen them work faster than traditional secondary shops.

OPERATIONAL VALUE POST-CLOSE. The continuation vehicle exists precisely because the sponsor wants to continue executing the same strategy with the same team. The sponsor already has their own operating playbook, value creation plan, and a well-established relationship with a management team that wants to avoid the operational disruption that comes with a change of control. A direct private equity firm seeking to add operational value post-close may encounter limited receptivity from a sponsor and management team that chose this structure precisely to maintain continuity.

GCM Grosvenor’s Approach

GCM Grosvenor’s approach to the continuation vehicle market reflects the firm’s position as one of the largest global allocators to private equity, with broad, deep relationships across the lower middle market, middle market, and small buyout segments. We believe we are uniquely positioned to capitalize on the GP-led market through our primary investing activities, which provide us with early looks at deals, historical perspective on companies and their sponsors, and help secure favorable allocations in oversubscribed situations.

Our sponsor-focused strategy in the CV market reflects a deliberate portfolio construction philosophy: to build a “best-of” portfolio of high-quality assets by partnering with top-performing sponsors across a diverse group of lead investors.

GCM Grosvenor has invested alongside 31 unique lead or co-lead investors in our GP-led deals.15 While many dedicated GP-led funds target concentrated portfolios of 10 to 15 deals, GCM Grosvenor targets 30 to 35 GP-led investments within its commingled, diversified secondary strategy. For an institutional investor seeking exposure to the continuation vehicle market through a single commitment, this diversification across sponsors, lead investors, and assets offers a meaningfully different risk-return profile than a concentrated portfolio built around a single investor’s deal flow and sector expertise.