Creating a Private Equity Program for Any Market Cycle

Past performance is not necessarily indicative of future results. No assurance can be given that any investment will achieve its given objectives or avoid losses. Unless apparent from context, all statements herein represent GCM Grosvenor’s opinion.

Investments in alternatives are speculative and involve substantial risk, including strategy risks, manager risks, market risks, liquidity risk, risks associated with exiting investments, and structural/operational risks, and may result in the possible loss of your entire investment. Please review the disclaimer following this report.

As the current market cycle matures, investors should look back at historical peaks – and ensuing fallouts – to better understand today’s private equity market. Here, we assess how the current environment resembles previous mature markets, and consider what we can learn from the similarities. Ultimately, we believe a well-designed private equity allocation program is the most critical factor needed to reap the benefits of the asset class, whatever the market environment. Investors who are considering a new or expanded investment in private equity should pay close attention to their strategic program design.

A Growing Need for Caution?

If you’re following the headlines, you may see some red flags waving across the investing landscape. For instance, there are signs of exuberance among mergers and acquisitions – namely high deal valuations and rising leverage for large-cap buyouts. Interest rates are signaling a slowdown on the horizon, with the yield curve’s flattening of late. Public equity markets are hovering at or near peak levels. Escalating trade tensions between the U.S. and China are pressuring the manufacturing and agriculture sectors, among others, and are contributing to a slowdown in global growth.

How do investors who are considering a new or expanded private equity program factor-in these red flags? It may be surprising, but our view is that short-term movements in the market environment should only have a small impact on a well-designed private equity program. Even in a mature market, we would urge new and expanding investors to focus first on their long-term investment program.

Lessons from the Last Market Peak

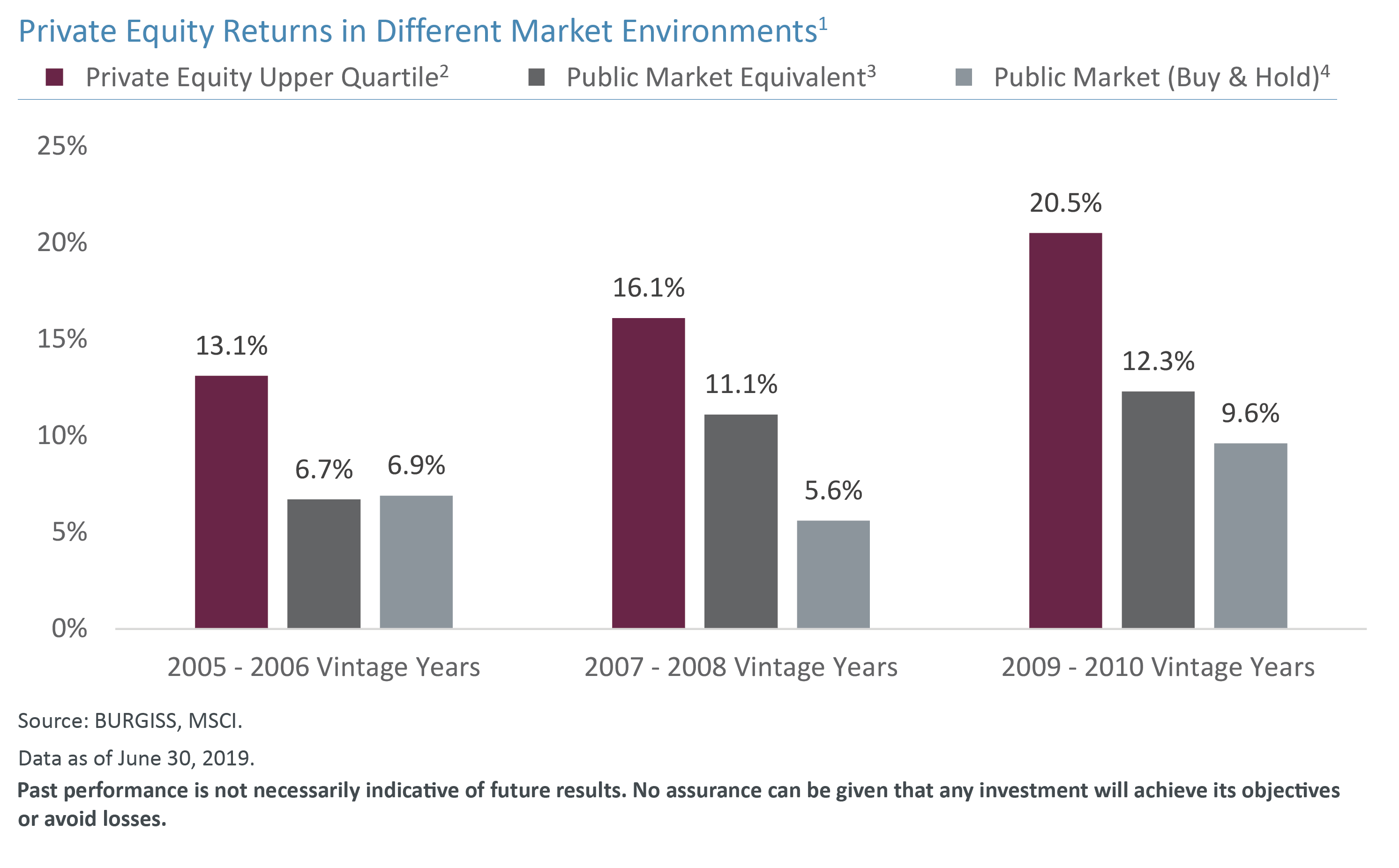

It is next to impossible to accurately call market peaks in the moment. This is especially true in more illiquid markets such as private equity. In hindsight, many 2005 and 2006 vintage private equity deals were done at peak levels preceding the financial crisis. Some investors who entered private equity at that time ultimately saw weaker internal rates of return (IRRs) on their investments. As a result, in some cases, new entrants and experienced investors chose to stop or dramatically slow their pace of deployment into private equity, and thus did not enjoy what turned out to be a fruitful investment environment post-crisis, as illustrated below.

However, not all investors of the period had the same experience. Some navigated that point of the market cycle just fine. Many of those who ultimately enjoyed better long-term performance shared some essential qualities in terms of how they designed their private equity programs and the actions they took in the periods following market peaks.

Opportunities Exist

We believe it is imperative to consider lessons-learned from previous cycles. For example, as was the case before the financial crisis, the deals that show the strongest signs of frothiness today tend to be concentrated in specific segments. Larger-cap leveraged buyouts are certainly exhibiting signs of exuberance. Similarly, fundraising for large- and mega-cap buyout funds has been much stronger than other segments of late.

We believe that it leaves a considerable range of opportunities with manageable valuations and deal terms. Small- and mid-cap, emerging managers, and targeted regional strategies are presenting different valuations and outlooks today than large-cap buyouts, though such opportunities may not be on the radar for many investors.

Mature market cycles are also an ideal time for tactical positioning with certain countercyclical categories. Restructuring and event-driven strategies, for instance, should be considered in times of uncertainty, so as to create balance in the portfolio. In today’s environment, we see attractive restructuring opportunities in European markets, where a variety of market and macro headwinds have had an impact on economic activity. Selected industry sectors in the US are also providing interesting restructuring opportunities. For example, the energy sector, where significant headwinds have led to severe dislocations, could be an additional source of tactical opportunities for well-positioned private equity managers.

Ultimately, for any disciplined approach aiming to avoid buying high and selling low, times of broader market stress may provide opportunities for investors to acquire fundamentally mispriced quality assets.

Importance of a Long-Term Outlook

Today, we see a range of investment opportunities and substantial evidence that, while we are not experiencing a replay of the ’05 and ’06 market environment, we should learn from it. Perhaps the most important takeaway for prospective private equity investors today: it’s a long-term asset class. It’s not an allocation that you jump in and out of depending on the environment. A short-term view of private equity is practically guaranteed to increase overall risk levels.

All of this begs the question of how investors may design the kind of balanced private equity program that will help them navigate the ups and downs of market cycles. We have identified five key steps.

Take the Long View

As discussed, a typical private equity program should be designed with a long-term horizon in mind, on the order of 10-15 years. The underlying investments of private equity are fundamentally medium- to long-term commitments. A smart allocation must align with the mechanics and characteristics of the asset class.

Taking the long view is also about spreading entry points over time. Just as investors are encouraged to use dollar-cost averaging in their retirement accounts, time-diversification offers a degree of risk mitigation to private equity programs.

Diversity Across Multiple Dimensions

Most institutions know they need to diversify public investments across many dimensions – by market-cap size, value/growth style, and geography, for example. But they may neglect to diversify their private equity allocations in the same way. A truly diverse private equity program spreads exposures not only across time and market caps, but by strategy (buyouts, venture, growth, distressed, and others) and by private equity manager size (large, small, emerging), for instance.|

Partner Strategically

In designing a private equity program, an investor must take care to conduct an objective evaluation of where the organization has skill and access – and where it does not. These gaps represent areas where a strategic partnership would be especially valuable to the organization.

The private equity world is one where access and expertise are the gatekeepers of profitable investments. In other words, top opportunities are frequently open to a select few who have the connections to the investments and the skill to take advantage of them.

In this category, we would include co-investments and strategic partnerships, which can broaden the opportunity set and also offer lower-fee investments. We would also consider accessing expertise in niche strategies or other value-add asset classes.

Create Thoughtful Policies and Procedures…and Stick to Them

When a market turns south, anxieties rise. Most institutions will have an instant increase in terms of their demand for information, transparency, and communication from their private equity investments and partners. We believe it is essential to prepare for these demands when initiating a program. All investors, new or experienced, should step back and consider what kind of policies and procedures would serve their institution not just in healthy market environments, but during periods of stress.

Communication and transparency can be a make-or-break factor. When investors are anxious and unable to obtain timely information about their investments, they are more likely to abandon programs or exit holdings at the worst possible moment. Effective monitoring techniques and policies are essential to the proper functioning of a long-term asset class, as well as to the management of the type of partnerships described here.

Design Tactical Choices Into the Program

We believe a balanced program that includes diversification across several strategies and assets will be well-positioned in almost any market environment. However, a program that provides for some degree of tactical freedom can have even better prospects for the long term. This allows a program to take advantage of current opportunities in niche areas such as real assets, purchases of non-performing loans (NPLs) or distressed assets, or at early stages of a market cycle in areas such as growth investments. These tactical moves can provide countercyclical balance to other parts of a private equity program while preserving a long-term orientation.

Importance of a Long-Term Outlook

The current market environment could eventually prove to have been a market peak – or it might not. We advise investors to step away from the headlines when considering their investment in private equity. Private equity investing requires a balanced viewpoint and a long horizon to reap value. Tactical investment freedom is valuable, but it is not the sole element that helps institutions to be successful in their private equity programs. For those looking to start or expand their investment in the asset class today, we believe thoughtful and balanced program design is the ultimate answer to navigating all market cycles.

RELATED NEWS AND INSIGHTS

Access Is Built, Not Bought: A Long-Term Approach to Middle-Market Private Equity

We explore how long-term relationships and disciplined execution drive differentiated access in middle-market co-investing.

Decoding the Secondary Middle-Market: What It Means and Why It Matters

We unpack how different managers define middle-market secondaries, why those definitions matter, and how thoughtful execution can turn complexity into opportunity.

Important Disclosures

Investments in alternatives are speculative and involve substantial risk, including strategy risks, manager risks, market risks, and structural/operational risks, and may result in the possible loss of your entire investment. Please review the disclaimer following this report.

1 Burgiss data based on published 2Q 2019 benchmark data downloaded on October 4, 2019. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indices or financial products. This report is not approved or produced by MSCI. No assurance can be given that any investment will achieve its objectives or avoid losses. Past performance is not necessarily indicative of any future results.

2 “Private Equity Upper Quartile IRR” represents the upper quartile net IRR since inception through June 30, 2019 for all buyout funds in the Burgiss Manager Universe with vintage years 2005-2006, 2007-2008 and 2009-2010, respectively.

3 “Public Market Equivalent” returns reflect the MSCI World (TR) Index using the Long-Nickels methodology and were obtained from Burgiss.

4 “Public Market (Buy and Hold)” represents the annualized rate of return for the MSCI World (TR) Index (Ticker: GDDUWI) as of year-end of the first year of each time period through June 30, 2019.

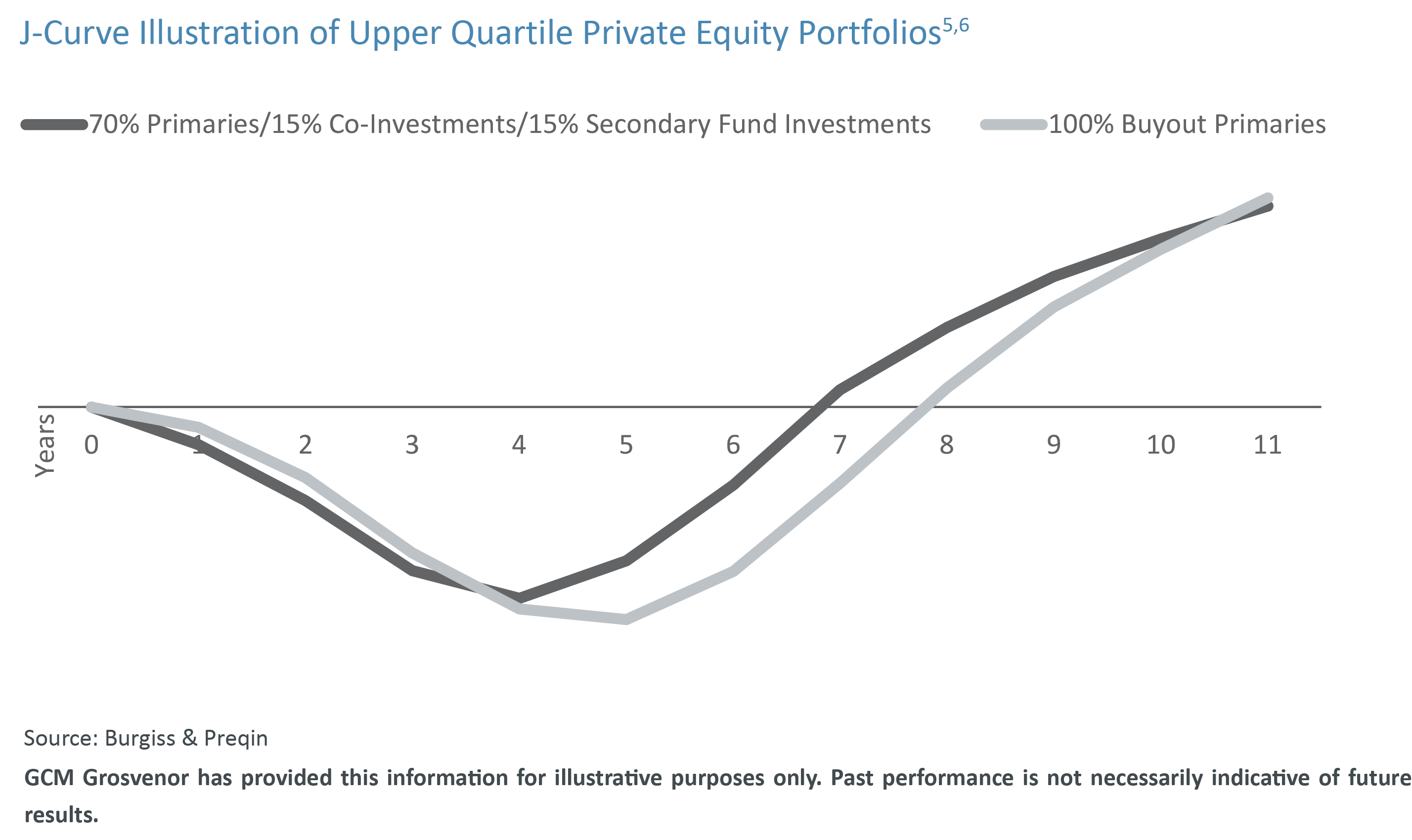

5 Illustrative portfolio consists of 52.5% primary buyout fund investments, 17.5% special situation primary fund investments, 15.0% co-investments and 15.0% secondary fund investments.

6 Private equity portfolios reflect upper quartile net multiple of invested capital for buyout funds, special situation funds, and private equity secondary fund portfolios with a vintage year of 2015 or prior as sourced from the Burgiss database. Burgiss data is based on published 2Q 2019 benchmark data downloaded on November 5, 2019. Additionally, the private equity portfolios reflect the upper quartile net multiple of invested capital for private equity co-investment portfolios with a vintage year of 2015 or prior as sourced from the Preqin database. Preqin data is based on latest available benchmark data downloaded on November 5, 2019.

The views expressed are for informational purposes only and are not intended to serve as a forecast, a guarantee of future results, investment recommendations or an offer to buy or sell securities by GCM Grosvenor. All expressions of opinion are subject to change without notice in reaction to shifting market, economic, or political conditions. The investment strategies mentioned are not personalized to your financial circumstances or investment objectives, and differences in account size, the timing of transactions and market conditions prevailing at the time of investment may lead to different results. Certain information included herein may have been provided by parties not affiliated with GCM Grosvenor. GCM Grosvenor has not independently verified such information and makes no representation or warranty as to its accuracy or completeness. GCM Grosvenor’s strategy definitions differ from those used by The Burgiss Group (“Burgiss”). GCM Grosvenor has used its best efforts to match each strategy with the appropriate Burgiss strategy but material differences may exist. Additional information is available upon request.