The secondaries market has emerged as a critical pillar of private equity, experiencing record-breaking activity in 2024 with deal volume on track to exceed $140 billion. This Q&A explores the key drivers behind this surge, the evolving dynamics of LP- and GP-led deals, and predictions for the road ahead. GCM Grosvenor shares insights into the market’s resilience, the factors shaping its future, and how the firm leverages its platform in seeking to capitalize on these opportunities.

This last year saw record-breaking deal volume in the secondaries market, and the current year is showing a similar positive trajectory. What do you consider the primary drivers of this surge, and do you believe these factors will continue to influence market strategies in 2025?

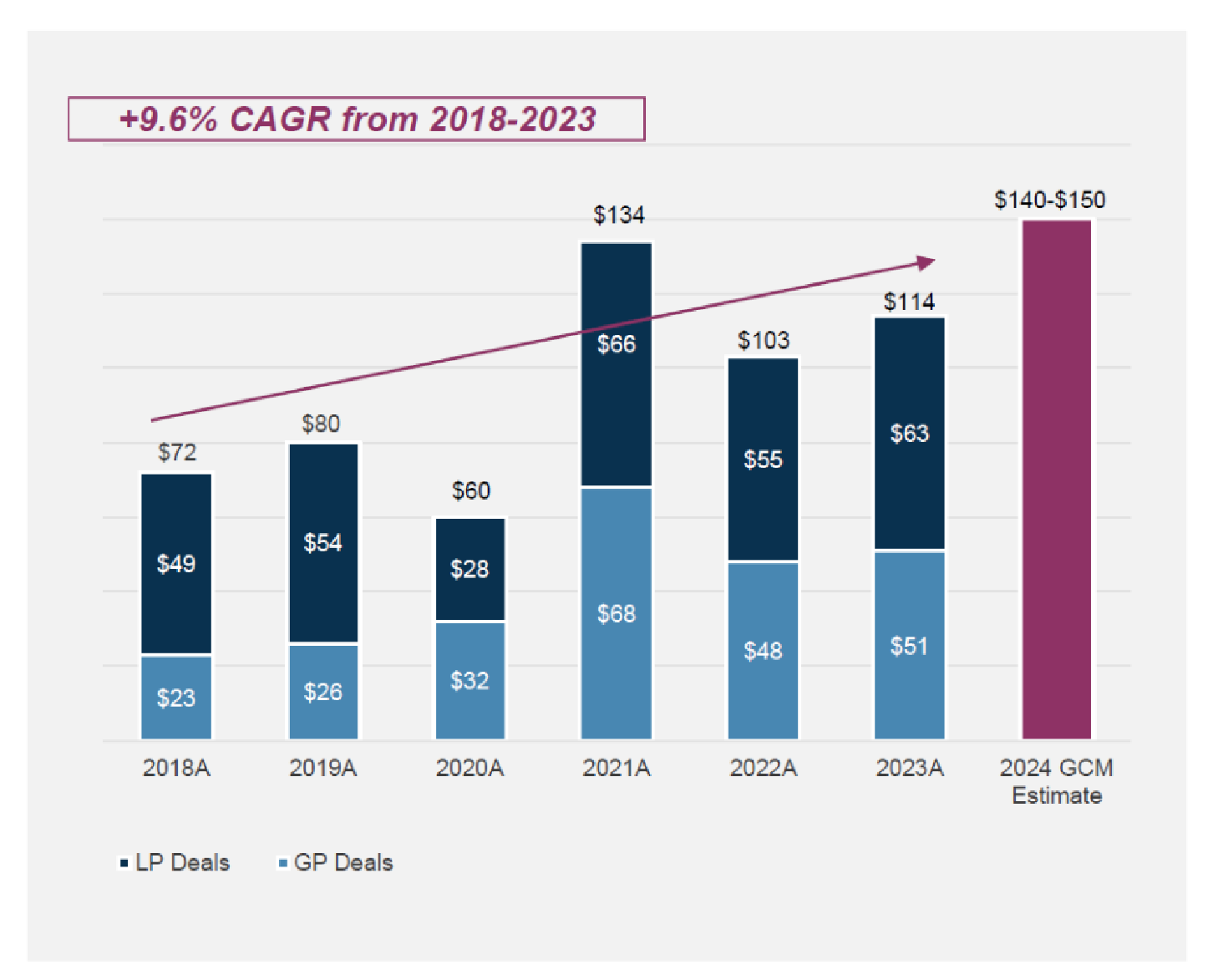

The first half of 2024 achieved record-breaking deal volume of approximately $70 billion,1 and our year end estimate (2024E) is on track to surpass $140 billion—marking the highest level ever observed in the secondaries market and representing a roughly 20%+ increase over 2023.

The sluggishness in the M&A and IPO markets throughout 2024 has resulted in limited distributions to underlying LPs, prompting institutions and PE sponsors to turn to the secondaries market for liquidity. This trend has driven a surge in volume for both the traditional LP-led secondaries and GP-led deals, building on the significant secular growth that the space has already seen over the last five years.

Looking ahead, for LP-led secondaries, tighter pricing over the past two years, driven by reduced economic uncertainty and the closing of larger secondary funds, is likely to attract more LP sellers in 2025. Similarly, on the GP-led side, sponsors are increasingly favoring continuation funds to retain high-performing assets, which is expected to sustain volume in the coming year as sponsors explore creative liquidity solutions.

While the slowdown in the M&A and IPO markets has provided a tailwind for the secondaries market, we anticipate sustained robust volume in the medium and long term due to the continued growth of the overall private equity market and the increased acceptance of secondary sales as a portfolio management tool. Since the secondary market is a derivative of the primary market, the high levels of primary fundraising over the past decade will naturally lead to greater secondary volume as investors continue to use the secondary market to generate liquidity or otherwise actively manage their private equity portfolios. Additionally, the growing unrealized value in funds and the advancing age of underlying portfolio companies held by PE funds will continue to support significant volume in the secondaries market for years to come. The average holding period for buyout funds has increased almost 50% since 2009,2 further contributing to the sustained demand and continued volume in the secondaries market.

TRANSACTION VOLUME DRIVEN BY GP-LED ACCELERATION

Secondary Transaction Volume ($b)

Data Source: Evercore FY 2023 Secondary Market Survey Results

1. Data Source: Evercore H1 2024 Secondary Market Review

2. Data Source: “Average Holding Period for Buyout Deals”; Preqin as of December 4, 2024

How would you compare the opportunity set for LP and GP-led deals over the next few years?

For LP-led secondaries, market dynamics are always evolving. Over the past two years, pricing for LP deals has steadily tightened, with the size of the discount influenced by various factors, including fund strategy. Buyout funds consistently command the highest prices, a trend that continued over the past year (93-98% of NAV).3

In addition to reduced economic uncertainty compared to two years ago, tighter pricing is likely driven by the substantial capital raised by secondary funds over the past 18 months, as well as, to some extent, capital raised by 40 Act evergreen funds. Pricing differences persist depending on the size of the portfolio offered for sale, with larger portfolios experiencing faster tightening as major secondaries players reach final closes on their funds and face pressure to deploy capital and mitigate the J-curve in their funds.

The quality of the manager also plays a key role in pricing. Increasingly, we are seeing more portfolios include “core” (i.e., typically high-quality) managers alongside “non-core” manager cleanups to increase the overall pricing of the portfolio.

GCM Grosvenor’s strategy of focusing on smaller portfolios—often cherry-picked from larger pools—and pursuing opportunities where we have a differentiated edge has historically provided, and may continue to provide, some insulation from the tightening pricing environment. We feel we are uniquely positioned to capitalize on secondary sales involving small and middle-market buyout funds, leveraging the strength of our private equity platform in this space.

For GP-led secondaries, the market remains under capitalized, and we expect this dynamic to continue in the foreseeable future. Despite new entrants and recent large fundraises, the GP-led market continues to be constrained by limited buy-side capital. That said, transactions involving the highest quality managers and companies continue to be oversubscribed, and securing an allocation to smaller deals remains highly competitive.

Thanks to the breadth of GCM Grosvenor’s platform and relationships, especially across the small and midmarket buyout space, we are often aware of continuation funds prior to their official launch. By highlighting our interest early, we can often gain access to oversubscribed vehicles.

What was once just a small segment of overall deal volume, primarily comprised of underperforming funds, GP-led transactions now account for almost half of secondary market volume and include some of the highest quality companies and sponsors. While there are several types of GP-led transactions (e.g., tender, strip sale, fund financing, etc.), continuation funds comprise approximately 80%+ of the GP-led market.4

Since the sponsor is already familiar with the asset and is typically self-selecting its best assets to hold for another value creation cycle, we expect these vehicles to experience lower volatility compared to buyout funds. While continuation funds are still a relatively new asset class, initial research has supported the thesis that single-asset continuation funds offer similar returns to buyout funds, but with lower volatility.5

As continuation funds have historically generated attractive returns, increased market interest should naturally drive further volume growth.

We believe having an existing relationship with the sponsor as a primary investor will continue to be a differentiating factor in both LP and GP-led deals. For LP secondaries, this can mean getting access to restricted processes and less available portfolio details. In GP-led deals, it can mean getting preferential allocations to over-subscribed deals. Based on our experience, managers of smaller funds are often more engaged in secondary transactions than those managing larger funds. This is primarily because smaller funds tend to have fewer investors, making each relationship more critical. These managers often place considerable value on whether the buyer is an existing investor or if the buyer’s organization will continue to be, or could become, a long-term partner. This consideration can also influence how forthcoming a manager is with information about the relevant portfolio during the secondary diligence process.

We routinely leverage this dynamic in our underwriting of both LP- and GP-led deals. GCM Grosvenor’s position in the market is distinct and well-suited to seeking to capitalize on the expected growth of the secondary market.

3. Data Source: PJT 3Q 2024 Secondary Market Insight

4. Data Source: Evercore H1 2024 Secondary Market Review

5. Data Source: Q2 2024 Continuation Fund Performance Report – Evercore Private Capital Advisory; HEC “Continuation Funds” Performance and Determinants White Paper, October 2024

Did the private markets experience the same level of volatility as the public markets over the past year?

While public markets have experienced significant volatility in recent years, private markets have been relatively stable due to their valuation methodology. Private equity managers typically calculate fair value quarterly, using public equity comparables, precedent transactions, and discounted cash flow models. Not only are private equity marks less frequent but sponsors often apply more conservative valuations – for example, using median comparable valuation multiples for an above average company, resulting in smoother valuations trends.

This “stickiness” in valuations can lead to discrepancies, with top-performing companies sometimes being undervalued on a fund’s books.

Lower volatility is one factor driving increased capital flows into the primary private equity funds and, by extension, increased secondary market volume.

What are your top three predictions for the secondary market over the next few years?

Continued Robust Growth in Volume – We estimate the secondaries market will reach $200 billion+ by 2028, (~12%+ CAGR from 2023).6

GP-Led Secondaries Will Remain Undercapitalized – Even with all the new entrants and increasing secondary fund sizes, the GP-led secondaries will remain undercapitalized and constrained by the amount of available buy-side capital. Nevertheless, we still expect the transactions involving the highest quality managers & assets to remain oversubscribed. GP relationships will continue to play a key role in getting an allocation for syndicate members.

Pricing For Smaller Deals Will Remain at Higher Discounts – As mentioned above, prices on LP-led secondaries are tightening, but more so at the larger end of the market. While prices still may tick up, we would anticipate smaller portfolios, and the ones that GCM Grosvenor is focused on, to be a bit more insulated. The smaller portfolios tend to be less competitive as information may not be shared as broadly, leading buyers to rely on their own information and they often tend to be too small for the larger players to target efficiently.

6. Data Source: Evercore H1 2024 Secondary Market Review