Access in a Capacity-Constrained Market

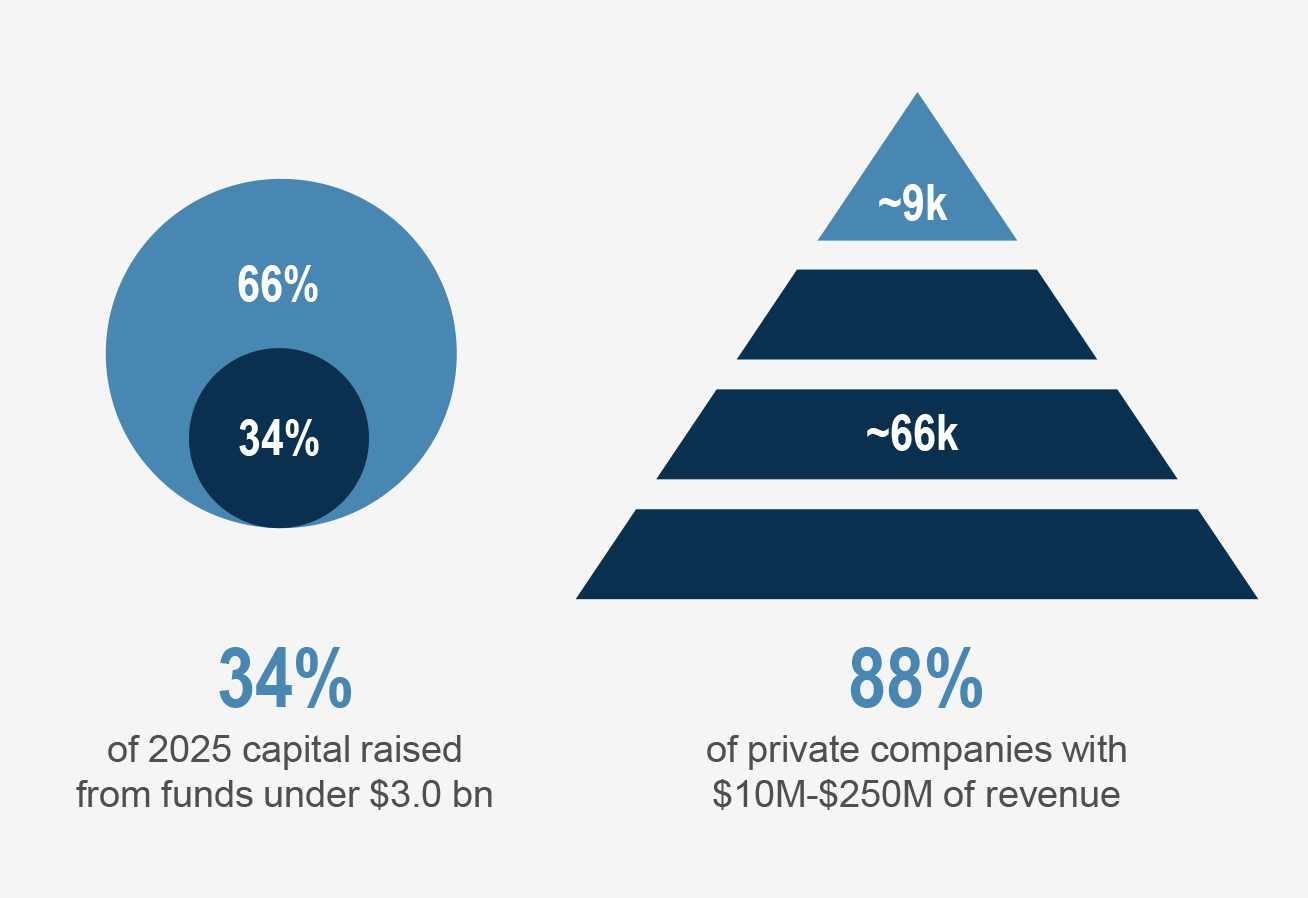

The middle market remains one of the most compelling segments of private equity. While most private companies fall within the middle market, a disproportionately smaller share of institutional capital is deployed there, creating a large and relatively underpenetrated opportunity set. These dynamics have supported lower entry multiples, more conservative leverage, a wider set of value creation levers, and multiple exit pathways over time.

As investors increasingly seek exposure in the middle market, many discover that top-performing middle-market managers have become capacity constrained. Established managers can be selective about whom they allow into their often oversubscribed funds.

In that context, access is less a function of size and more a reflection of relationships built over time – who engaged early, remained active as the firm scaled, and engaged in different ways throughout its evolution. For investors, these dynamics increasingly influence not only access, but also portfolio construction, deployment consistency, and the potential repeatability of attractive risk-adjusted outcomes across cycles.

Since inception, the middle market has been core to GCM Grosvenor’s private equity practice, anchored by a market-leading commitment to Small and Emerging Managers (SEM). The following perspective outlines how durable and preferred access is built over time, and how this approach is expressed in GCM Grosvenor’s middle-market co-investment platform today.

The Middle Market Represents a Large but Underpenetrated Segment of Private Equity

Source: CapIQ: Data as of March 3, 2026; represents North American private companies only. Includes all sectors. Revenue based on latest fiscal year. Note: Middle Market is defined as companies with $10 million to $250 million in annual revenue.

In the middle market today, access is increasingly relationship-driven.

A Unique Sourcing Engine

Sustained access to high-quality middle-market opportunities is the cumulative result of time, consistency, deep networks, experienced teams, and early conviction.

Early engagement with managers builds enduring relationships, particularly in the middle market where repeat partnerships are highly valued. As managers scale and increase fund sizes, access typically tightens. New investors — regardless of scale — are left competing for residual capacity. These relationships serve as a differentiated sourcing engine, contributing to sustained access to future funds and co-investment opportunities.

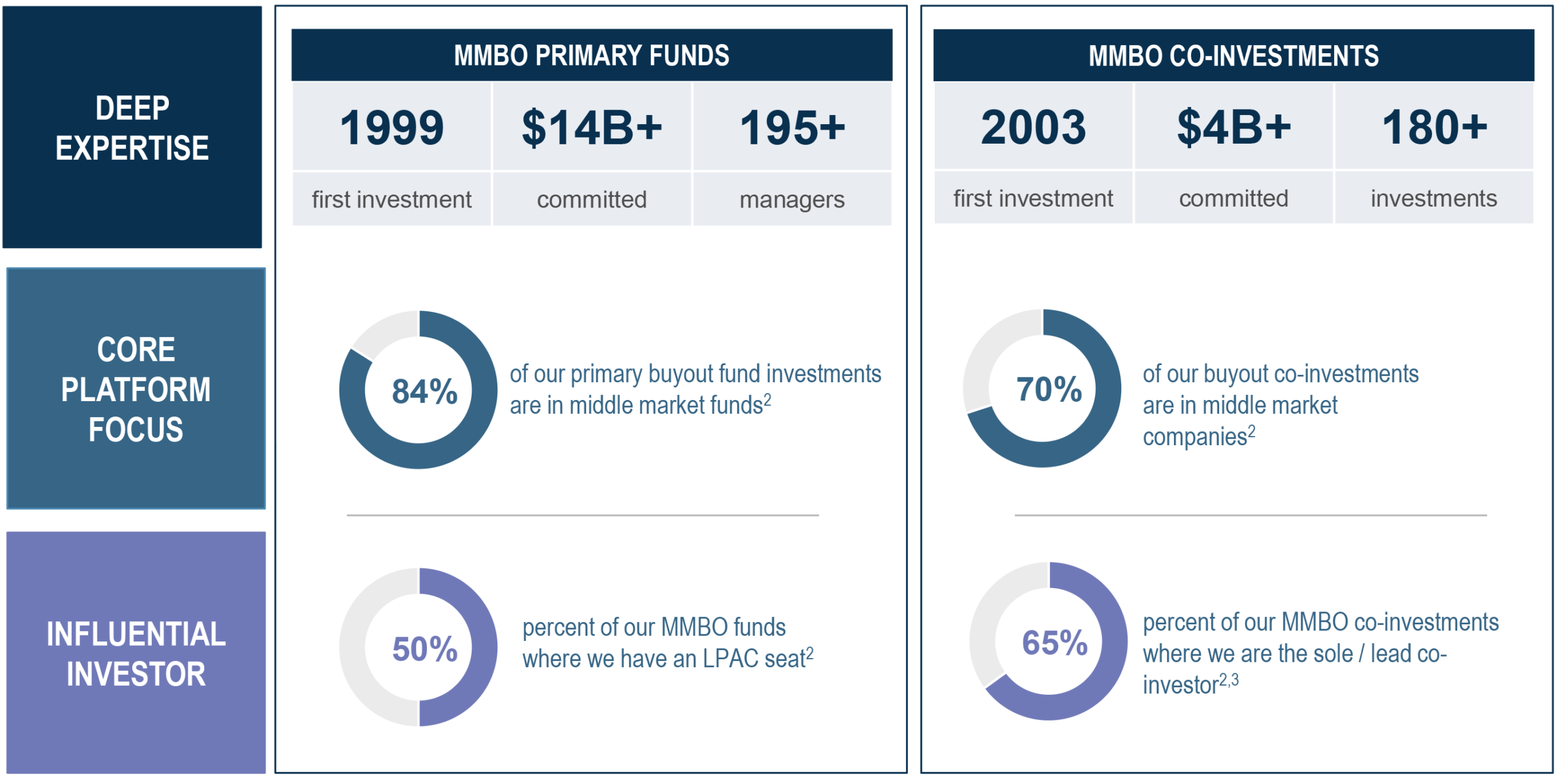

GCM Grosvenor’s middle-market practice has been built around this orientation for more than 25 years. Through its Small and Emerging Manager platform and repeat underwriting across fund generations, the firm has developed relationships with over 195 middle-market managers and committed over $14 billion to middle-market buyout funds, reflecting a long-term focus on continuity across cycles rather than episodic access.

Our Middle-Market Focus: We are one of the most experienced and influential investors in the middle-market buyout (“MMBO”)1 space

GCM Grosvenor’s long-standing focus on middle-market buyouts reflects early engagement and a true partnership approach with GP relationships across market cycles.

Source: Data as of September 30, 2025. Note: All co-investment statistics reflect data on buyout co-investments executed since 2009.

Value-Add Co-Investor

In the middle market, access alone does not translate into outcomes without disciplined evaluation and execution. In contrast to post-close syndications commonly used in large buyouts, middle-market managers often require equity co-investment partners to close transactions or enable pursuit of larger deals. As a result, middle-market managers prioritize co-investors that can underwrite efficiently, provide certainty of close, and engage constructively throughout the process.

In the middle market, co-investment capital is often integral to securing and financing an investment—making execution from co-investment partners critical.

Middle-market managers value institutional co-investors capable of taking on MNPI and efficiently co-underwriting transactions alongside them. They can serve as value-added partners by enhancing GPs’ credibility with sellers and financing sources through support letters, equity commitment letters (ECLs), and participating in management meetings during transaction processes.

Conclusion

Access in middle-market private equity is not incidental—it is built deliberately over time through early GP engagement, repeat underwriting, and consistent execution.

In a market where demand for middle-market exposure continues to outpace capacity, early access can increasingly shape not only opportunity flow, but also the consistency of capital deployment and investment outcomes across cycles.

Importantly, realized experience across multiple vintages informs underwriting standards, execution discipline, and downside management—key considerations for institutional investors assessing the repeatability and durability of a co-investment platform.

Since 2003, GCM Grosvenor has deployed over $4 billion in over 180 middle-market co-investments.

For investors, partnering with a platform like GCM Grosvenor—built on long-standing relationships, experience-informed underwriting, and disciplined execution—can provide diversified exposure to the middle market, through its access to some of the highest quality buyout sponsors.