Key Takeaways from GCM Grosvenor’s Annual Infrastructure Investor Day

Infrastructure is entering a new phase of global expansion as artificial intelligence, electrification and industrial modernization require extraordinary expenditure to meet rapidly accelerating demand. At GCM Grosvenor’s annual Infrastructure Investor Day in London, investors and industry partners gathered to discuss the evolving market backdrop and the implications for infrastructure investing over the coming decade.

Chief Investment Officer Fred Pollock outlined a constructive — though increasingly selective — outlook for the asset class. While macro uncertainty, higher financing costs and geopolitical volatility require careful consideration, the outlook for infrastructure investments remains supported by the same critical characteristics that have supported infrastructure for decades – durable demand, high barriers to entry, structural capital shortfalls and growing physical constraints tied to power, connectivity and permitting.

Markets Are Repricing Expectations, Not Retreating From Risk

Markets continue to adjust to a materially different interest rate environment than investors enjoyed for over a decade, post GFC. Expectations for more aggressive monetary easing have given way to a “higher-for-longer” outlook as economic activity continues to demonstrate resilience despite persistent inflation.

At the same time, geopolitical tensions and evolving trade dynamics have contributed to greater dispersion across sectors, financing markets and regional economies. While headline equity indices have remained relatively resilient, underlying volatility across asset classes has increased meaningfully.

Pollock noted that investor expectations surrounding the long-term cost of capital have shifted considerably over the past year, contributing to repeated repricing across both public and private markets.

Against that backdrop, market performance has become increasingly uneven beneath the surface. Sector leadership has narrowed, rate expectations have repeatedly reset, and investors have become more selective.

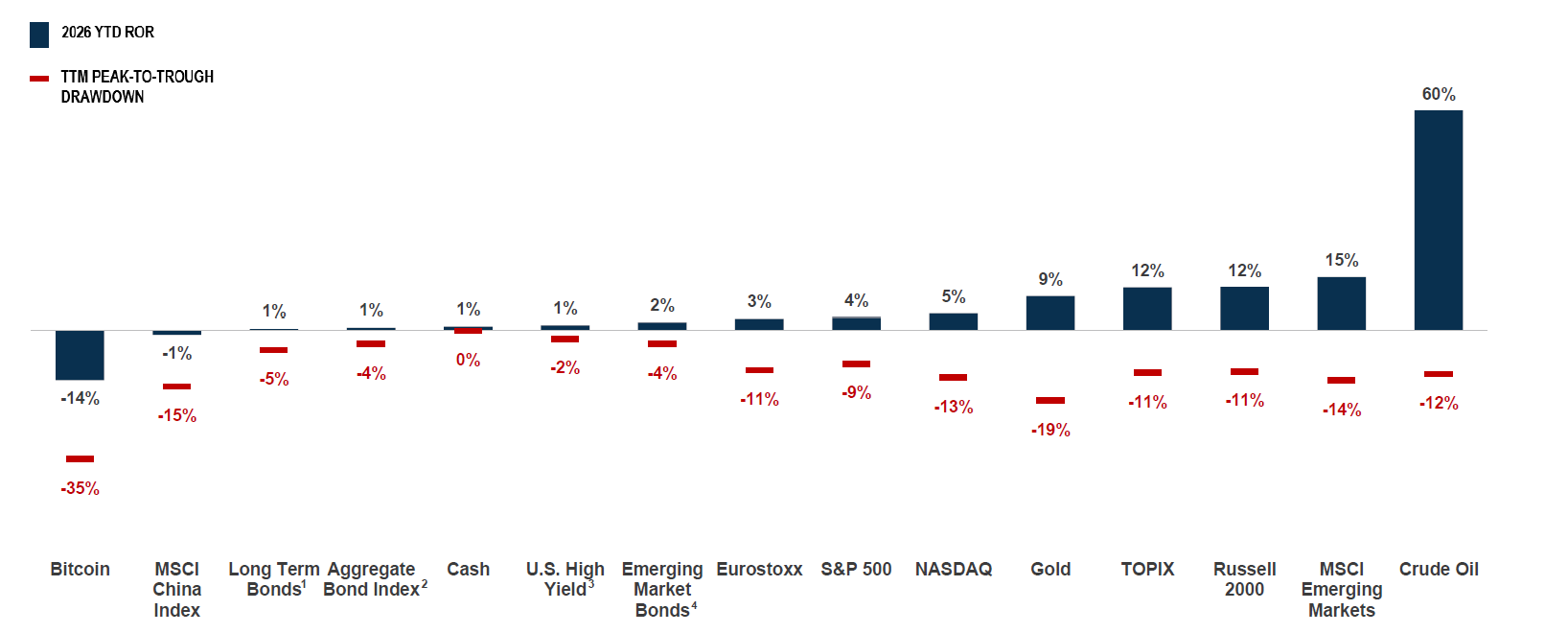

YTD Market Performance

Source: Bloomberg Finance, L.P. Performance shown as of April 21, 2026.

- Long Term Bonds: Bloomberg S. Treasury 20+ Year Total Return Index

- Aggregate Bond Index: Bloomberg Global-Aggregate Total Return Index Value Unhedged

- S. High Yield: Bloomberg US Corporate High Yield Total Return Index Value Unhedged

- Emerging Market Bonds: P. Morgan EMBI Global Diversified Index

Past performance is not necessarily indicative of future results. No assurance can be given that any investment will achieve its objectives or avoid losses.For illustrative purposes only.

Importantly, periods of heightened uncertainty have not yet translated into broad-based market dislocation. Financing conditions for high-quality assets remain constructive, particularly across sectors supported by durable cash flows and long-term secular demand.

That resilience has extended into portions of the infrastructure market, where significant capital needs continue to intersect with rising demand for energy, digital connectivity and industrial modernization.

Pollock emphasized that the current environment increasingly reflects a transition away from a broadly beta-driven market toward one characterized by greater dispersion, underwriting selectivity, and differentiated execution capability.

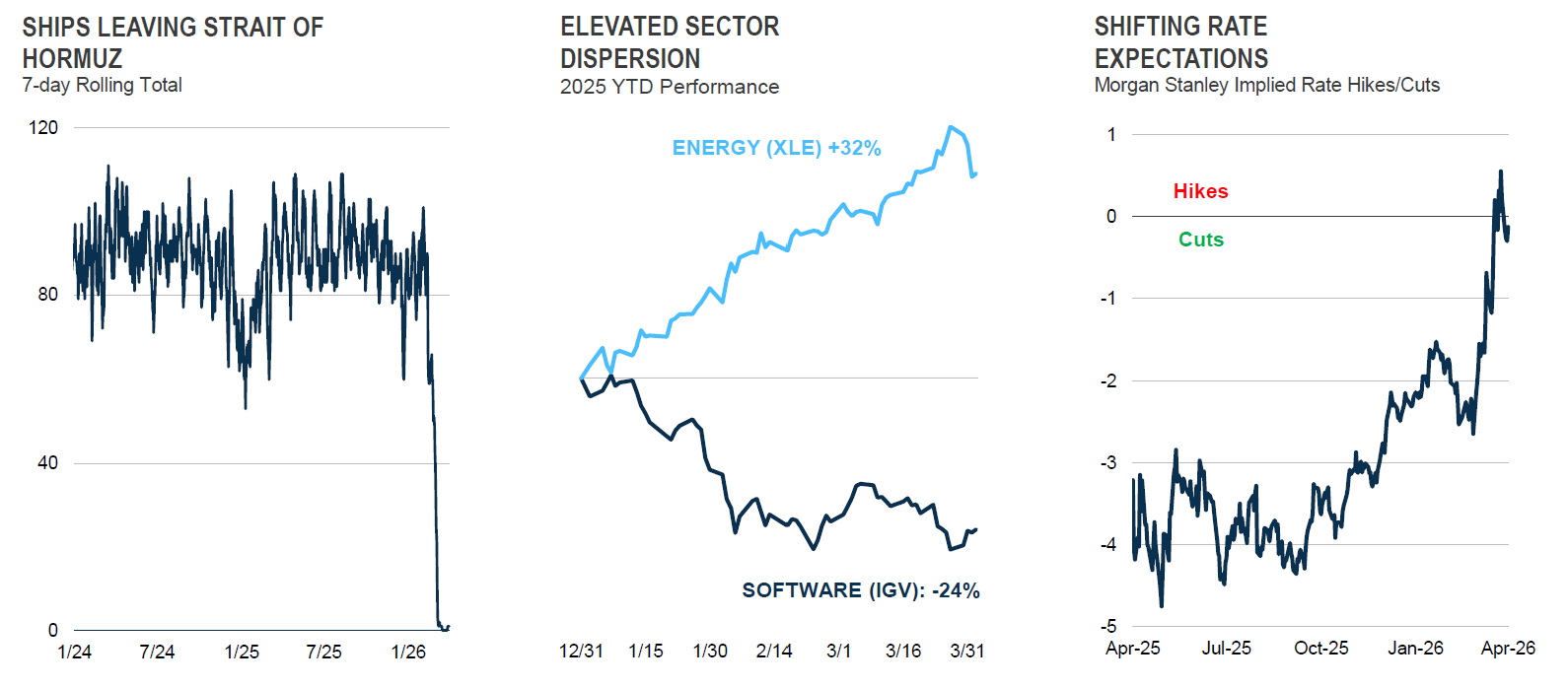

Evolving Market Backdrop

Source: Bloomberg Finance, L.P. Data as of March 31, 2026.

For illustrative purposes only.

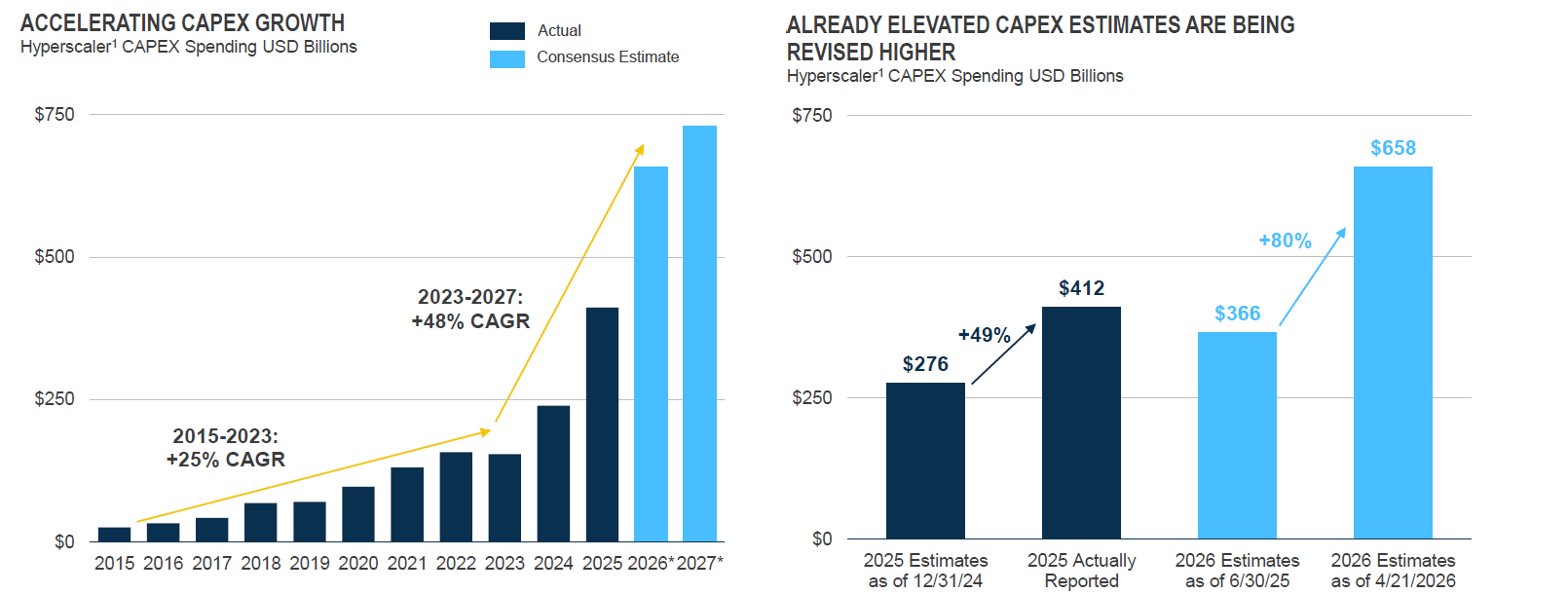

AI Is Driving One of the Largest Capital Spending Cycles in Modern History

One of the most significant themes discussed during the event was the scale of the global AI investment cycle now underway and its implications for infrastructure markets.

Pollock noted that hyperscaler capital expenditures continue to accelerate at a pace that has repeatedly exceeded expectations, driving growing demand across data centers, power generation, transmission infrastructure and digital connectivity assets.

The intensity of this competition for energy and infrastructure is perhaps best illustrated by Alphabet’s $4.75 billion acquisition of Intersect Power, announced in December 20251, the first time a hyperscaler has moved to directly own a major renewable energy developer rather than rely on power purchase agreements.2 The deal is designed to give Google a team that can develop, build, and generate power directly alongside data centers, bypassing the lengthy timelines companies typically face when connecting new facilities to the electrical grid. This kind of vertical integration into the energy supply chain signals a meaningful escalation in how the largest technology companies are approaching the infrastructure buildout required to power AI at scale.

While demand dynamics such as these often result in periods of overbuilding, the broader demand trends will undoubtedly produce a significant amount of productive, near-term infrastructure investment, coupled with some opportunistic investing in the future.

For infrastructure investors, this distinction is important. Unlike sectors facing disruption risk from AI, infrastructure is critically necessary for the proliferation of AI, and therefore infrastructure assets are positioned as enabling components of the broader transformation.

Forecasts for AI-related infrastructure spending have continued moving materially higher even after multiple upward revisions, underscoring the scale and persistence of anticipated demand growth.

AI Capital Expenditures

AI CapEx growth remains a dominant investment narrative with significant economic and market impact

Source: Bloomberg Finance, L.P, S&P Global CapIQ. Data as of April 21, 2025. For illustrative purposes only.

1 Hyperscalers defined as Alphabet, Amazon, Meta, Microsoft, and Oracle

The implications extend well beyond digital infrastructure alone. Rising computing intensity is increasingly driving secondary demand for power generation, transmission upgrades, cooling systems and broader industrial supply chains required to support large-scale AI deployment.

Pollock observed that the scale and speed of current AI-related capital expenditures may prove historically significant, particularly given the interconnected infrastructure systems required to support long-term computing demand.

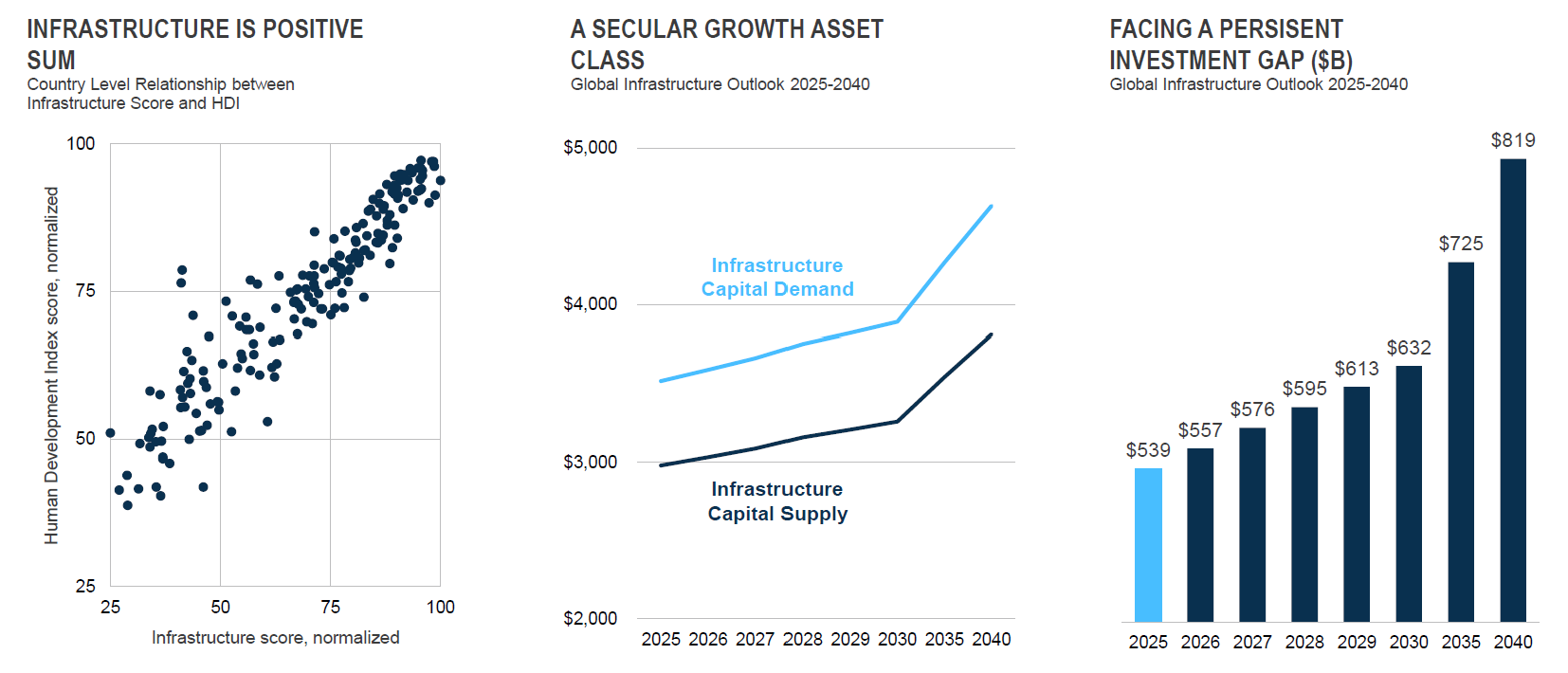

Infrastructure’s Positioning Remains Strong

Infrastructure remains unusually well-positioned within the broader private markets landscape due to the simultaneous expansion of multiple secular demand drivers. Infrastructure continues to benefit from the emergence of entirely new categories of demand tied to digitalization, electrification, industrial modernization and AI-related development.

Pollock noted that the unique correlation between continuing expansion of the infrastructure opportunity set, even as institutional appetite for the asset class has grown materially.

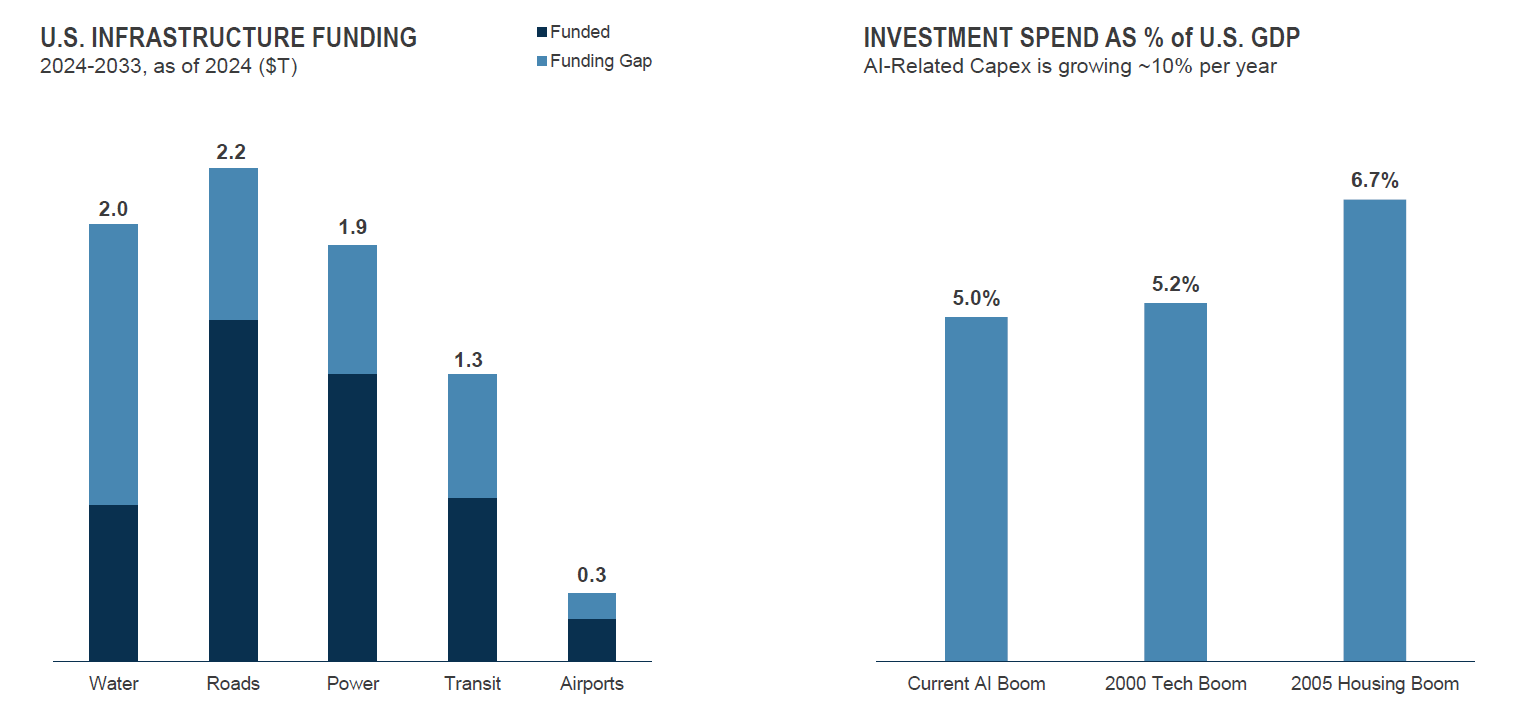

Long-term capital demand remains supported by the essential nature of infrastructure assets, coupled with persistent funding gaps across all major segments of the market, including energy, transportation, grid modernization and digital infrastructure systems globally.

U.S. Infrastructure Demand — Funding Gaps and AI Investment as % of GDP

Source: American Society of Civil Engineers, KKR, U.S. Bureau of Labor Statistics, Bloomberg Finance, L.P. For illustrative purposes only.

Over the coming decade, those funding requirements are expected to intersect with rising demand for power-intensive technologies, industrial electrification and continued modernization of aging infrastructure networks.

The result is an environment in which infrastructure assets increasingly sit at the intersection of ongoing capital needs and secular economic transformation.

Attractive Long-Term Infrastructure Supply/Demand Dynamics (2025–2040)

Source: Global Infrastructure Outlook, World Bank, World Economic Forum, Human Development Report Office. For illustrative purposes only.

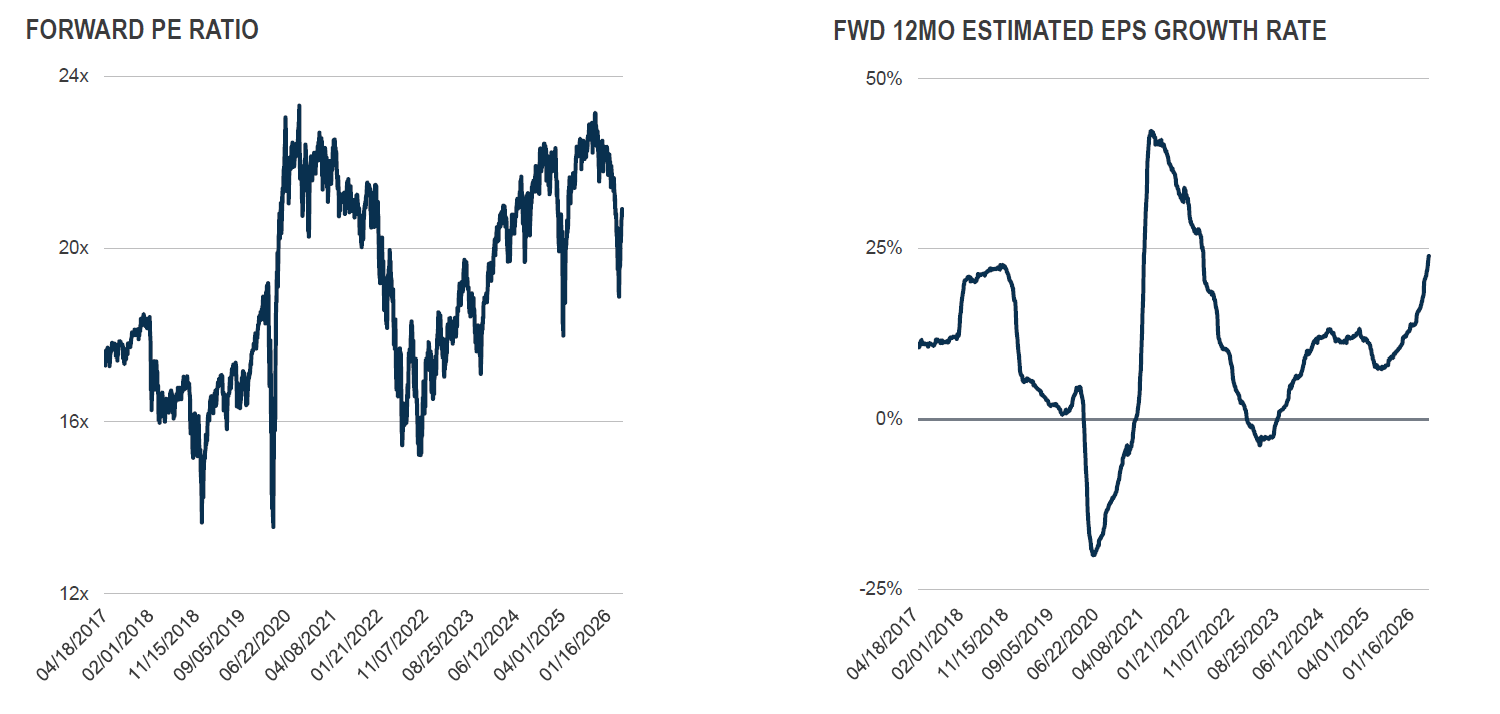

Selectivity Is Becoming More Important Than Scale

Despite the constructive long-term backdrop, the current market environment increasingly rewards underwriting discipline, asset selectivity and operational execution.

In general, valuations across portions of both public and private markets remain elevated relative to prevailing financing conditions, limiting the likelihood that broad market exposure alone will drive returns over the coming decade. Instead, investors may increasingly need to rely on differentiated sourcing, operational value creation, and disciplined capital deployment when looking to generate attractive risk-adjusted returns.

In that environment, scale alone may prove less important than the ability to navigate complexity, underwrite asset-level risk and access opportunities supported by long-duration secular demand drivers.

Pollock emphasized that the current environment increasingly favors alpha generation over broad beta exposure, particularly as higher financing costs create greater dispersion across asset quality and execution capability.

The combination of elevated valuations and ambitious earnings expectations continues to reinforce the importance of selectivity across both public and private markets.

Equity Valuations and Earnings Growth Expectations

Source: Bloomberg Finance, L.P. For illustrative purposes only. Past performance is not necessarily indicative of future results.

The Next Constraint May Be Physical, Not Financial

Looking ahead, one of the most important infrastructure investment themes may be the growing gap between capital availability and physical capacity.

Pollock suggested that the primary constraints on AI-related infrastructure development have increasingly shifted away from financing availability and toward access to power, transmission capacity, land, permitting and community acceptance.

Large-scale data center development, in particular, is beginning to place growing pressure on regional power grids, water systems and local infrastructure networks. Over time, those constraints may become increasingly economically relevant as developers and hyperscalers compete for limited access to critical infrastructure inputs.

The result may be an environment in which physical scarcity — rather than capital scarcity — becomes one of the defining characteristics of next-generation digital infrastructure investing.

A Constructive — but More Complex — Long-Term Outlook

Despite continued macro uncertainty and geopolitical volatility, the long-term infrastructure backdrop remains supported by several converging secular forces, including AI adoption, electrification, digitalization and the ongoing need to modernize aging infrastructure systems globally.

At the same time, the opportunity set is becoming increasingly complex. The next phase of infrastructure investing may depend less on identifying areas of demand — which appear abundant across many sectors — and more on determining where physical capacity can realistically scale alongside capital deployment.

Pollock noted that infrastructure is increasingly positioned not simply as a defensive asset class, but as a foundational enabling layer of future economic growth.

Assets located at the intersection of compute, power availability, connectivity and permitting capacity may ultimately define the next phase of infrastructure investment opportunity globally.