Access Is Built, Not Bought: A Long-Term Approach to Middle-Market Private Equity

We explore how long-term relationships and disciplined execution drive differentiated access in middle-market co-investing.

Past performance is not necessarily indicative of future results. No assurance can be given that any investment will achieve its given objectives or avoid losses. Unless apparent from context, all statements herein represent GCM Grosvenor’s opinion.

Select risks include: market risk, macroeconomic risk, liquidity risk, interest rate risk, and operational risk.

The private investing landscape has evolved greatly over the past few decades. Traditionally, investors looking for exposure to private equity and infrastructure entered the market through primary funds offered by core managers. As the landscape grew and matured, investors began investing beyond their “bulge bracket” funds, seeking the performance, diversification, and economic benefits offered by specialist and emerging managers, as well as through co-investments.

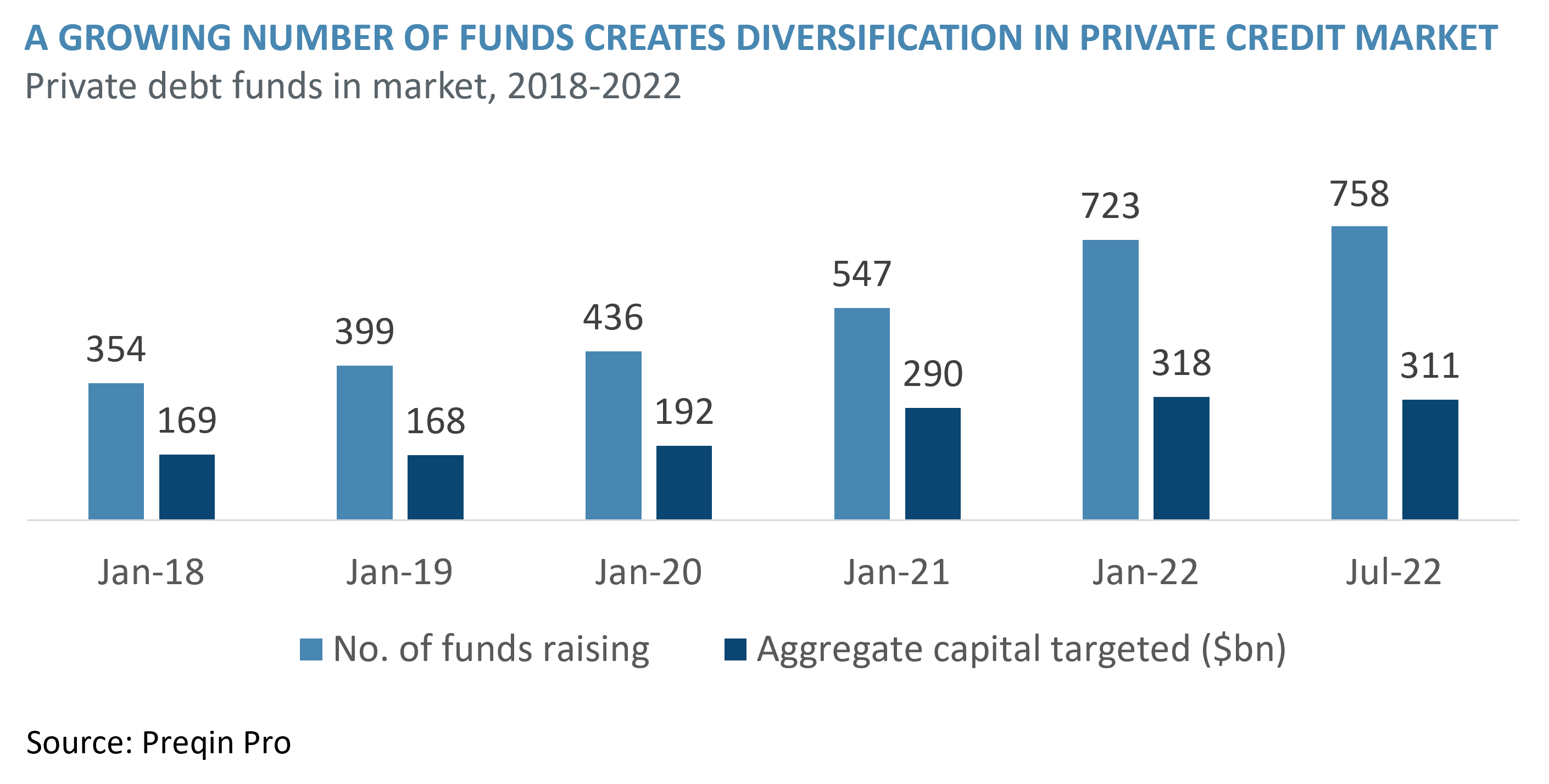

We are seeing a similar trend in private credit. While large direct lending firms make up most of investors’ private credit exposure, there has been a shift towards specialist managers and an emerging opportunity for credit co-investments.

Predictably, many investors are now seeking the potential for structural alpha, fee savings, and increased returns offered by credit co-investing. But given that co-investing in private credit is a relatively new and somewhat esoteric investment approach, there are unique elements that we believe contribute to a successful program.

Here, we look at the benefits of credit co-investing and explore what we believe to be the elements for success for those seeking to integrate co-investing into their credit allocations.

We believe there is a strong rationale for credit co-investing for several reasons:

The broad universe of private credit opportunities extends beyond the often-vanilla direct lending that is typical of most private credit investments.

There is flexibility in not being limited to a single credit strategy, which is particularly important during periods of market volatility.

There are favorable economics associated with a reduced total layer of fees, which can lead to better risk-adjusted returns than private credit alternatives.

Here, we look at the benefits of credit co-investing and explore what we believe to be the elements for success for those seeking to integrate co-investing into their credit allocations.

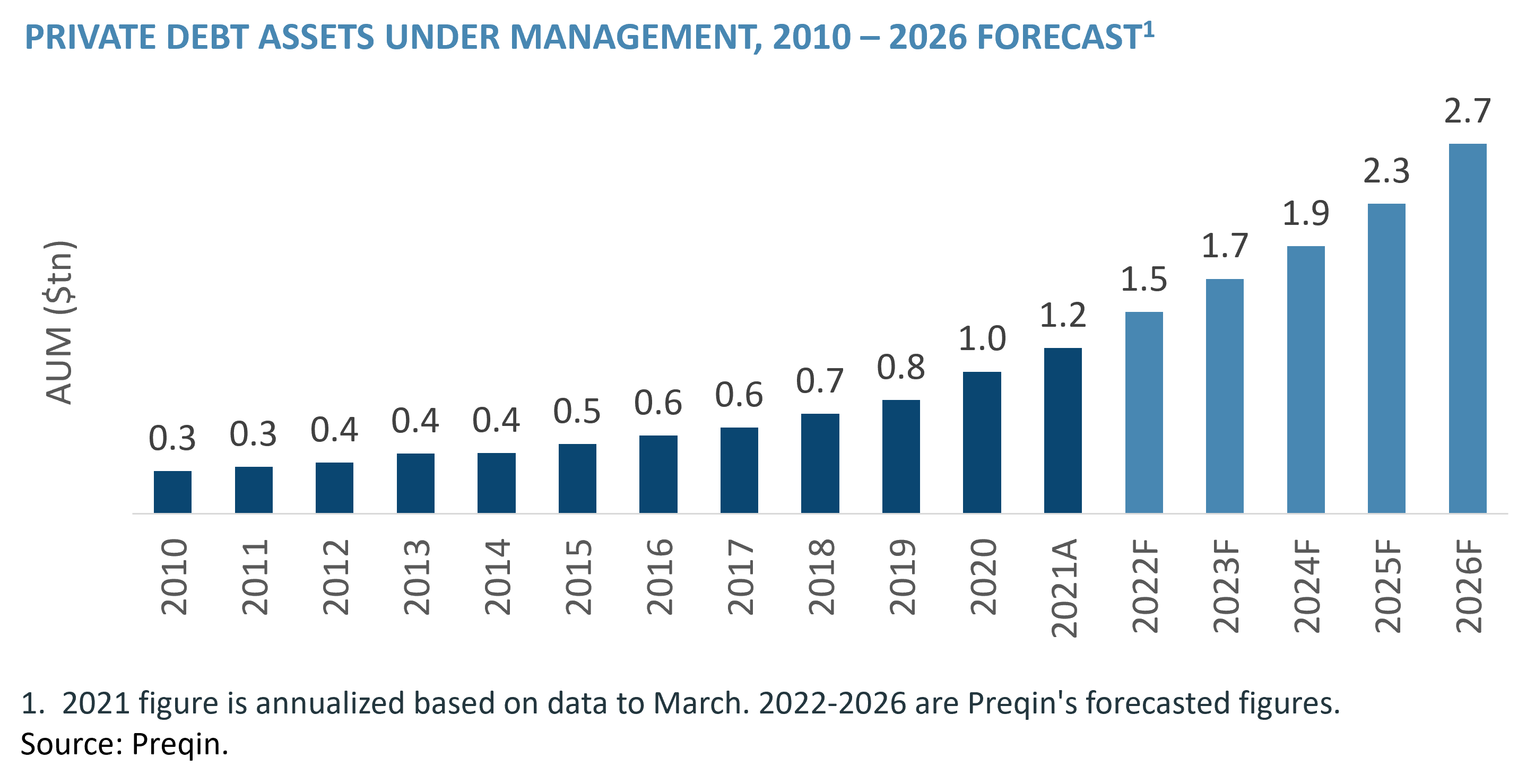

Allocations to private credit have grown in recent years. Continued growth is expected, as more investors see the benefits of adding it to their programs as they seek to decrease their risk appetite.

The benefit of layering-in co-investments allows investors to grow their existing private credit exposure more quickly with enhanced efficiency, while acting as an important diversifier. Given the current state of heightened volatility and uncertainty, we expect the trend to continue.

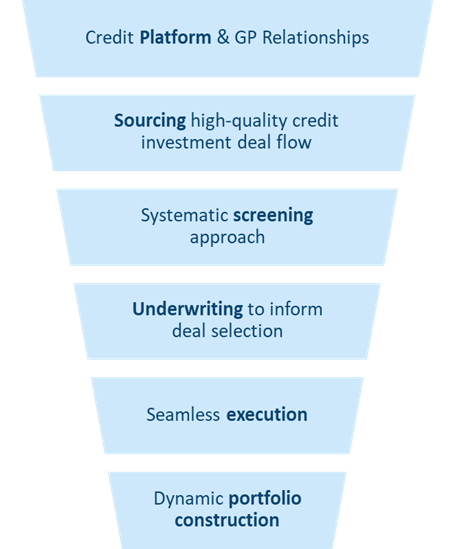

There are several key attributes and/or areas of expertise that we feel are crucial for an investor or advisor to successfully implement a credit co-investing program.

Investment platform

A prospective investor should have a broad scale, “open architecture” investment platform with many potential co-investment partners and a wide breadth of coverage across markets, geographies, and capital structures.

Sourcing

A healthy pipeline of deal flow is critical. An investor must not only develop many relationships with credit managers but also deep relationships to achieve “first-call” status. Doing so will create efficiencies (e.g., through quick yes/no decisions) and can provide access to capacity-constrained opportunities. An existing manager, sponsor, or partner is often a good place to start when sourcing credit co-investments.

Screening

It is challenging in any asset class to find the highest alpha producers, and credit is no different. When narrowing the funnel of opportunities, investors are seeking sponsors who are aligned with their desired risk/return profile. Finding that “sweet spot” is a challenge, but we believe an investor or advisor with a strong network can achieve it.

Underwriting

To successfully underwrite credit co-investments, we believe it takes years of experience and a high degree of skill in direct investing to avoid adverse selection. We also feel that a trust-but-verify approach is best – one that includes independent diligence while leveraging a co-investment partner’s work.

Execution

Because of the broad range of investment securities, types, and regions involved, implementing credit co-investments can be challenging. It’s our view that an investor should have a full suite of internalized capabilities, which includes prime brokerage relationships, ISDAs, traders, legal, compliance, tax, and other specialties that, when kept in-house, can significantly increase the speed of deal execution that is often critical to accessing an opportunity.

Portfolio Construction

Last, portfolio management of credit co-investments to meet an investor’s optimal risk/return preferences is vital. We believe it takes requisite levels of skill and experience to create a diversified portfolio that properly manages various risk factors and incorporates hedging components where needed.

At GCM Grosvenor, we feel that we are one of very few asset managers with the requisite investment platform, sourcing capability, investment implementation options, and track record to sufficiently partner with investors seeking private and alternative credit, particularly co-investing.

We explore how long-term relationships and disciplined execution drive differentiated access in middle-market co-investing.

We examine how GCM Grosvenor has successfully identified and capitalized on private equity co-investment opportunities, even in a challenging market environment.

Important Disclosures

For illustrative and discussion purposes only.

No assurance can be given that any investment will achieve its objectives or avoid losses. Past performance is not necessarily indicative of future results.

The information and opinions expressed are as of the date set forth therein and may not be updated to reflect new information.

Investments in alternatives are speculative and involve substantial risk, including strategy risks, manager risks, market risks, and structural/operational risks, and may result in the possible loss of your entire investment. The views expressed are for informational purposes only and are not intended to serve as a forecast, a guarantee of future results, investment recommendations, or an offer to buy or sell securities by GCM Grosvenor. All expressions of opinion are subject to change without notice in reaction to shifting market, economic, or political conditions. The investment strategies mentioned are not personalized to your financial circumstances or investment objectives, and differences in account size, the timing of transactions, and market conditions prevailing at the time of investment may lead to different results. Certain information included herein may have been provided by parties not affiliated with GCM Grosvenor. GCM Grosvenor has not independently verified such information and makes no representation or warranty as to its accuracy or completeness.

GCM Investments UK LLP (“GCMUK”) has been made aware of fraudulent schemes targeting members of the public in Spain.

Unauthorised individuals are falsely claiming to represent GCMUK and are misusing the firm’s name and publicly available information in connection with fake investment opportunities.

These scams are sophisticated and deliberately misleading. They may involve the use of real GCMUK employee names and may imitate the tone, format, and branding of genuine GCMUK communications.

Please note:

GCMUK does not offer financial services or investment products to retail clients, either directly or through third parties. You can verify GCMUK’s regulatory status and permissions on the UK Financial Conduct Authority (FCA) Register at register.fca.org.uk

If you are based in Spain and believe you have been contacted by a fraudster claiming to represent GCMUK, please take the following steps:

You may also report online fraud to the Spanish National Police or Civil Guard via the computer crime reporting service at www.policia.es.

GCM Investments UK LLP (“GCMUK”) ha tenido conocimiento de estafas dirigidas al público en España.

Personas no autorizadas afirman falsamente representar a GCMUK y están haciendo un uso indebido del nombre de la empresa y de la información disponible públicamente en relación con oportunidades de inversión falsas.

Estas estafas son sofisticadas y deliberadamente engañosas. Pueden implicar el uso de nombres reales de empleados de GCMUK e imitar el tono, el formato y la marca de las comunicaciones auténticas de GCMUK.

Tenga en cuenta lo siguiente:

GCMUK no ofrece servicios financieros ni productos de inversión a clientes minoristas, ni directamente ni a través de terceros. Puede verificar el estado regulatorio y los permisos de GCMUK en el Registro de la Autoridad de Conducta Financiera del Reino Unido (FCA) en register.fca.org.uk

Si reside en España y cree que ha sido contactado por un estafador que dice representar a GCMUK, siga los siguientes pasos:

También puede denunciar el fraude online a la Policía Nacional o la Guardia Civil española a través del servicio de denuncia de delitos informáticos en www.policia.es.

GCM Investments UK LLP (“GCMUK”) has been made aware of fraudulent schemes targeting members of the public in France.

Unauthorised individuals are falsely claiming to represent GCMUK and are misusing the firm’s name and publicly available information in connection with fake investment opportunities.

These scams are sophisticated and deliberately misleading. They may involve the use of real GCMUK employee names and may imitate the tone, format, and branding of genuine GCMUK communications.

Please note:

GCMUK does not offer financial services or investment products to retail clients, either directly or through third parties. You can verify GCMUK’s regulatory status and permissions on the UK Financial Conduct Authority (FCA) Register at register.fca.org.uk.

If you are based in France and believe you have been contacted by a fraudster claiming to represent GCMUK, please take the following steps:

You may also report online scams through the French government’s Pharos platform at www.internet-signalement.gouv.fr.

GCM Investments UK LLP (“GCMUK”) a été informée de l’existence de stratagèmes frauduleux visant le grand public en France.

Des personnes non autorisées prétendent faussement représenter GCMUK et utilisent abusivement le nom de la société et des informations accessibles au public dans le cadre de fausses opportunités d’investissement.

Ces escroqueries sont sophistiquées et délibérément trompeuses. Elles peuvent impliquer l’utilisation des noms réels d’employés de GCMUK et imiter le ton, le format et l’image de marque des communications authentiques de GCMUK.

Remarque:

GCMUK n’offre pas de services financiers ni de produits d’investissement à des clients particuliers, que ce soit directement ou par l’intermédiaire de tiers. Vous pouvez vérifier le statut réglementaire et les autorisations de GCMUK dans le registre de la Financial Conduct Authority (FCA) du Royaume-Uni à l’adresse register.fca.org.uk.

Si vous êtes basé en France et pensez avoir été contacté par un fraudeur prétendant représenter GCMUK, veuillez suivre les étapes suivantes :

Vous pouvez également signaler les escroqueries en ligne via la plateforme Pharos du gouvernement français à l’adresse www.internet-signalement.gouv.fr.

ご注意

・当社代表取締役の駒田智彦(もしくはその秘書を名乗るもの)が、LINE等のSNSやメール等を通じて金融商品への投資をご案内・勧誘することはございません。

・不審なメールのリンク先には絶対にアクセスしないようご注意ください。

・GCM Grosvenorの日本法人であるGCMインベストメンツ株式会社は、Webページを開設しておりません。また、Instagram、LineといったSNSにおいても公式ページは開設しておりません。

GCM Investments UK LLP (GCMUK) has been made aware of fraudulent schemes targeting members of the public in the United Kingdom.

Unauthorised individuals are falsely claiming to represent GCMUK and are misusing the firm’s name and publicly available information in connection with fake investment opportunities.

These scams are sophisticated and deliberately misleading. They may involve the use of real GCMUK employee names and may imitate the tone, format, and branding of genuine GCMUK communications.

Please note:

GCMUK does not offer financial services or products to retail clients, either directly or through third parties. You can verify GCMUK’s regulatory status and permissions on the Financial Conduct Authority (FCA) Register at register.fca.org.uk.

If you are based in the UK and believe you have been contacted by a fraudster claiming to represent GCMUK, please take the following steps:

Investor Scam Alert

Unauthorized individuals are impersonating Winston Chow in scams targeting investors, particularly in Malaysia. He does not solicit investments directly in Asia. If you are contacted by someone claiming to be him outside of official channels, please report it to local authorities.

For verification or further information, please contact: [email protected]

Investor Scam Alert

GCM Grosvenor L.P. and its affiliated entities (collectively, “GCMG”) have been made aware of fraudulent schemes currently targeting members of the public in Malaysia and Hong Kong, in which unauthorised individuals are falsely claiming to represent GCMG in connection with purported investment opportunities.

These fraudulent individuals are believed to be actively promoting false investment opportunities, often involving mobile applications, through the unauthorised use of GCMG’s name, brand, corporate logo, and other identifying materials. We have also received reports that these parties may be distributing fabricated business cards, hosting online webinars, creating WhatsApp groups, and arranging personal video calls to simulate legitimacy. These scams are sophisticated and deliberately misleading, frequently involving the use of real GCMG employee names and imitating the style, tone, and presentation of genuine GCMG communications.

GCMG has no presence, operations, or authorised representatives in Malaysia. GCMG does not offer any investment schemes, products, or mobile applications targeted at Malaysian investors, either directly or indirectly.

While GCMG maintains a legitimate presence and employs personnel in Hong Kong, these scams are entirely unauthorised and unrelated to any genuine activities conducted by GCMG or its employees in the region.

Position of GCMG

GCMG has neither authorised nor endorsed any such solicitations and takes this matter seriously. We have reported some of these incidents to the relevant regulatory and enforcement authorities in Malaysia, and are doing the same in Hong Kong, including notifying the Hong Kong Police and the appropriate financial regulators. GCMG will continue to assist with their investigations.

GCMG is actively monitoring these developments and reserves all rights to take legal action against any party found misusing its name, brand, or intellectual property.

While these reports currently centre on activity in Malaysia and Hong Kong, the methods used may be replicated in other jurisdictions. GCMG continues to monitor for similar risks globally.

Unauthorized individuals are impersonating Winston Chow in scams targeting investors, particularly in Malaysia. He does not solicit investments directly in Asia. If you are contacted by someone claiming to be him outside of official channels, please report it to local authorities.

For verification or further information, please contact: [email protected]

We offer clients a broad range of tailored solutions across strategies, including multi-strategy, macro, relative value, long/short equity, quantitative strategies, and opportunistic credit. Levaraging our large scale and presence in the industry, we are able to offer clients preferntial exposure to hard-to-access managers and seek to obtain terms that can drive economic and structural advantages.