Finding Opportunity in the Secondary Market Amid Dislocation

Past performance is not necessarily indicative of future results. No assurance can be given that any investment will achieve its given objectives or avoid losses. Unless apparent from context, all statements herein represent GCM Grosvenor’s opinion.

Select risks include: risks related to the lack of a liquid, transparent market for secondary investments, performance risk, and risks related to sourcing investments.

The global pandemic has touched every company, investment, and market, but in different ways. Here, we offer our perspectives on the current state of the secondary market and share ways to potentially capitalize on this once-in-a-cycle secondary opportunity.

We are in a unique position in the current market. We believe we will see a wave of secondaries opportunities driven by both limited partner sellers and GP-led situations."

Brian Sullivan, Managing Director, Private Equity Investments

How has the pandemic affected secondaries

As the scope of the global coronavirus pandemic became widespread in late February, public markets tumbled. Domestic large-cap indexes were down around 20% for the first quarter, while small-cap indexes averaged closer to down 30%. Private investments could suffer a similar decline, possibly even greater, depending on the specific assets and leverage involved. The continued global shutdown has continued into the second quarter, resulting in a more significant impact on operating performance. Second-quarter valuations of private equity holdings could continue the downward trend and come in lower than Q1 2020 marks in many cases.

We can characterize the market backdrop in the second quarter coming out of the first quarter’s severe dislocation with a few broad strokes:

+ Large bid/ask spreads for asset transactions

+ Broad-based need for liquidity across both GPs and LPs

+ Increased structured solutions amid atypical markets

Large Bid/Ask Spreads for Asset Transactions

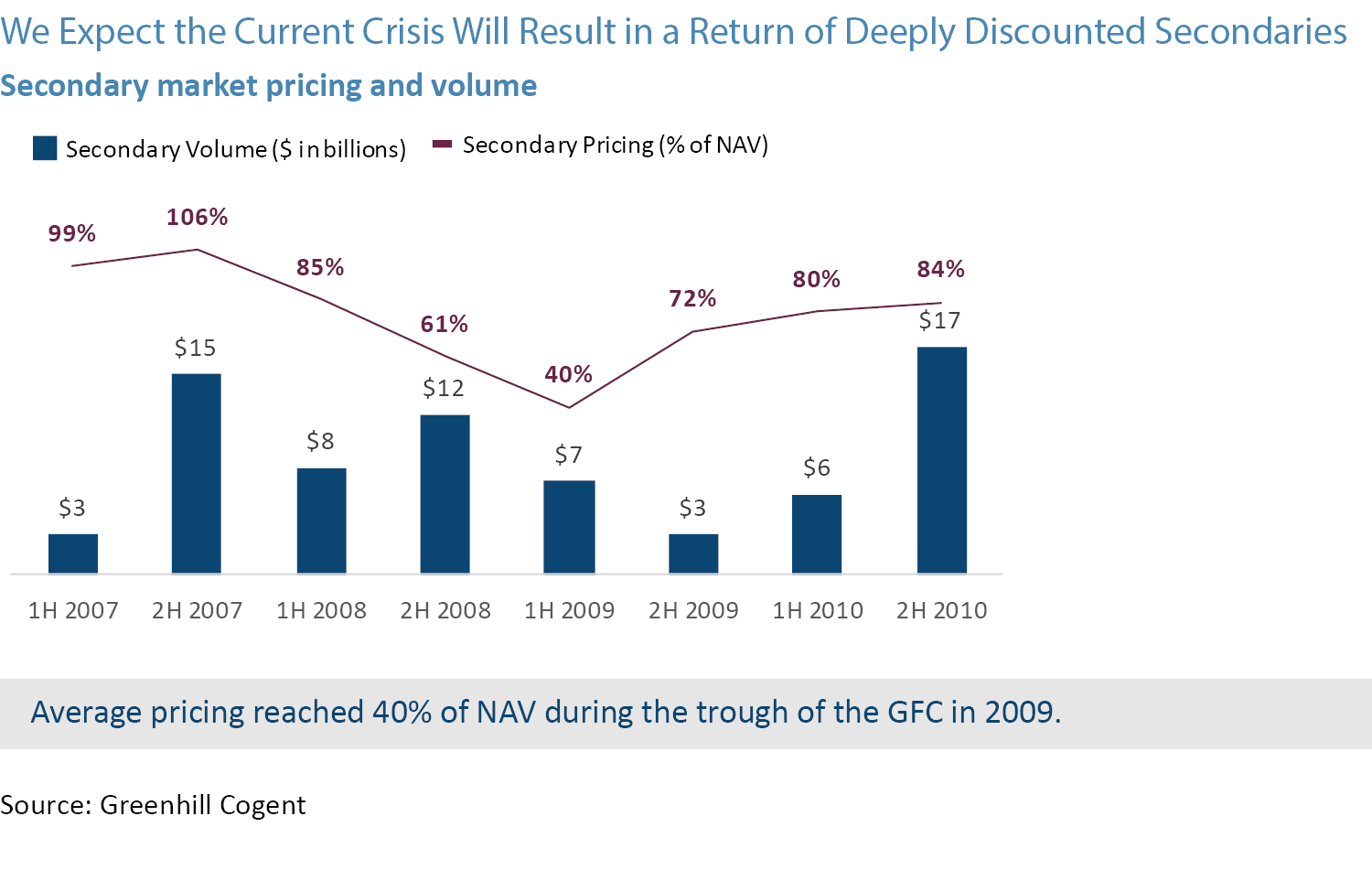

Following the decline of asset values, a significant bid/ask spread lingers across the secondary marketplace in the interim period before or until GPs revalue their portfolios. Published year-end 2019 valuations are outdated. A seller would have to accept a 20%-40%+ discount to transact just to account for the public market movements, terms that are optically grim, even if they are economically accurate (and could generate immediate liquidity). We expect bid/ask spreads to narrow once the decline in valuations, operational performance, and outlook are reflected in PE valuations.

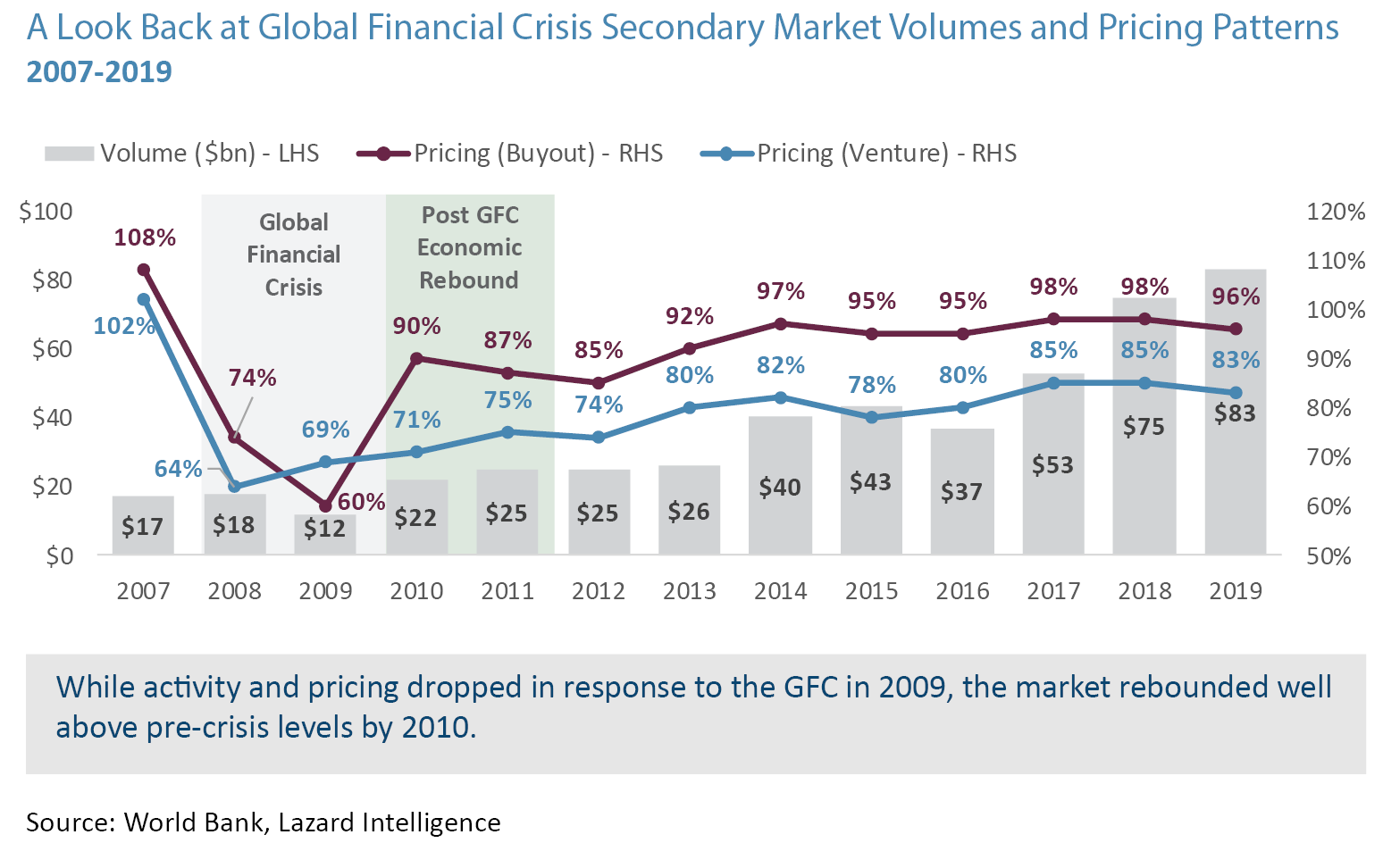

Besides pricing, we believe secondary transaction volumes will initially decline due to the friction caused by the pricing gaps. The pandemic puts entire industries in limbo as the next steps for public health remain in question. When we consider that a typical traditional secondary sale takes 3-6 months to complete in healthy economic environments, a backdrop of medium-term uncertainty is a major execution headwind. Given these factors, we expect traditional secondary sales will decline significantly in the first half of 2020, but are expected to pick up late this year and rebound in 2021-2022, as a result of both deferred and new liquidity considerations just as they did during and following the Global Financial Crisis.

Broad-Based Need for Liquidity Among Both GPs and LPs

Pressure to Raise Liquidity for GPs and LPs

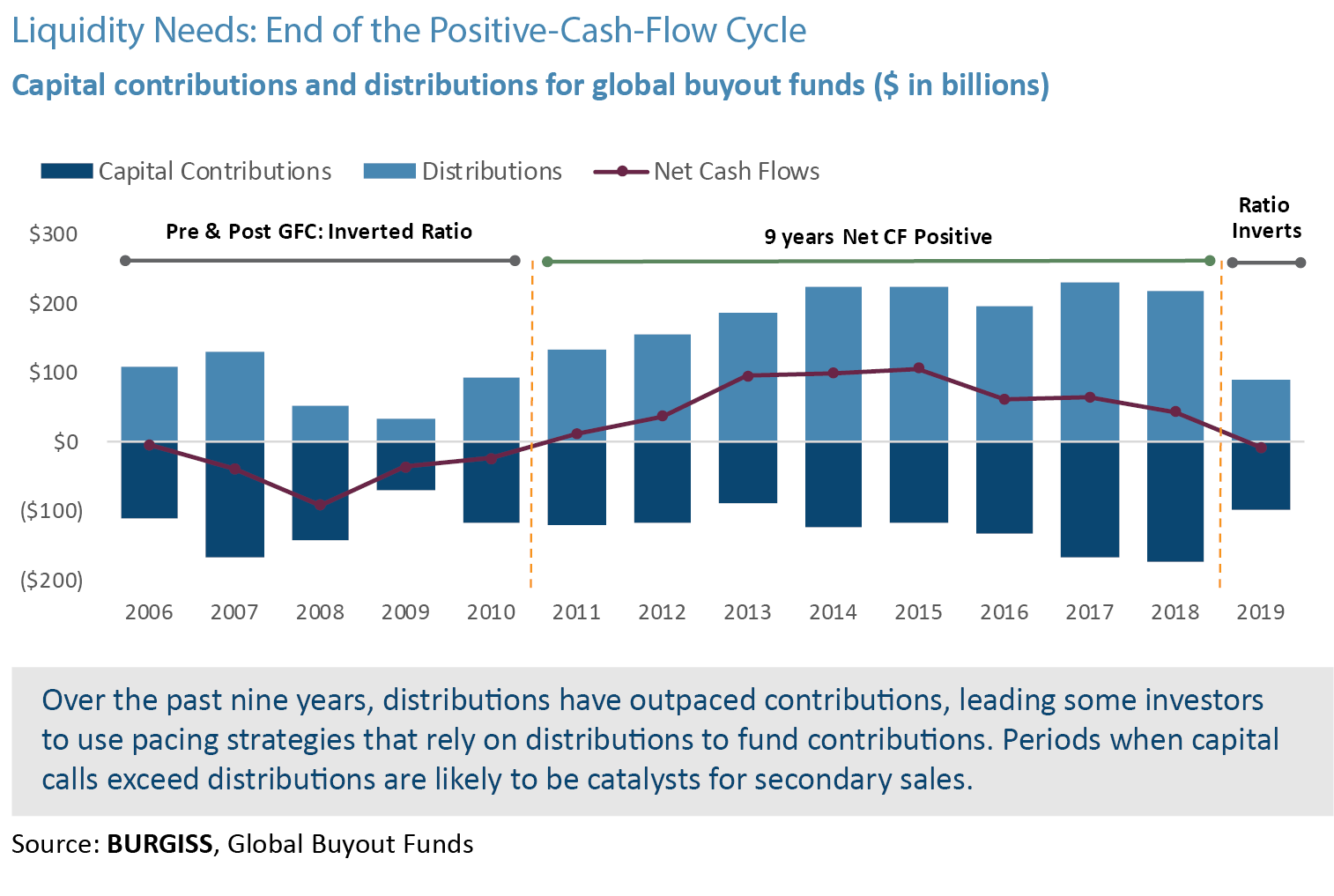

Net cash flows for LPs are expected to plummet in the short-term, and several forces are driving demand for capital at the GP level. GPs may need capital to shore up the balance sheet of portfolio companies under pressure; fund working capital or pay off credit facilities; or execute opportunistic follow-on acquisitions, capturing a rare buying opportunity for coveted investments. Meanwhile, exit opportunities often dry up in downturns, causing distributions to slow substantially.

For LPs, evaporating cash flows are not the only trend. Many investors are likely to face pressure from the denominator effect – as public market values fall, but private holdings stay flat due to the normal valuation lagA, private equity allocations are likely to appear bloated on a relative basis. Even for investment boards that understand the nature of the problem, the appearance is often enough to push investors to trim allocations. This effect could linger for an extended period as investment committees and boards consider their options and revise portfolio allocations and projections.

Opportunistic Viewpoint

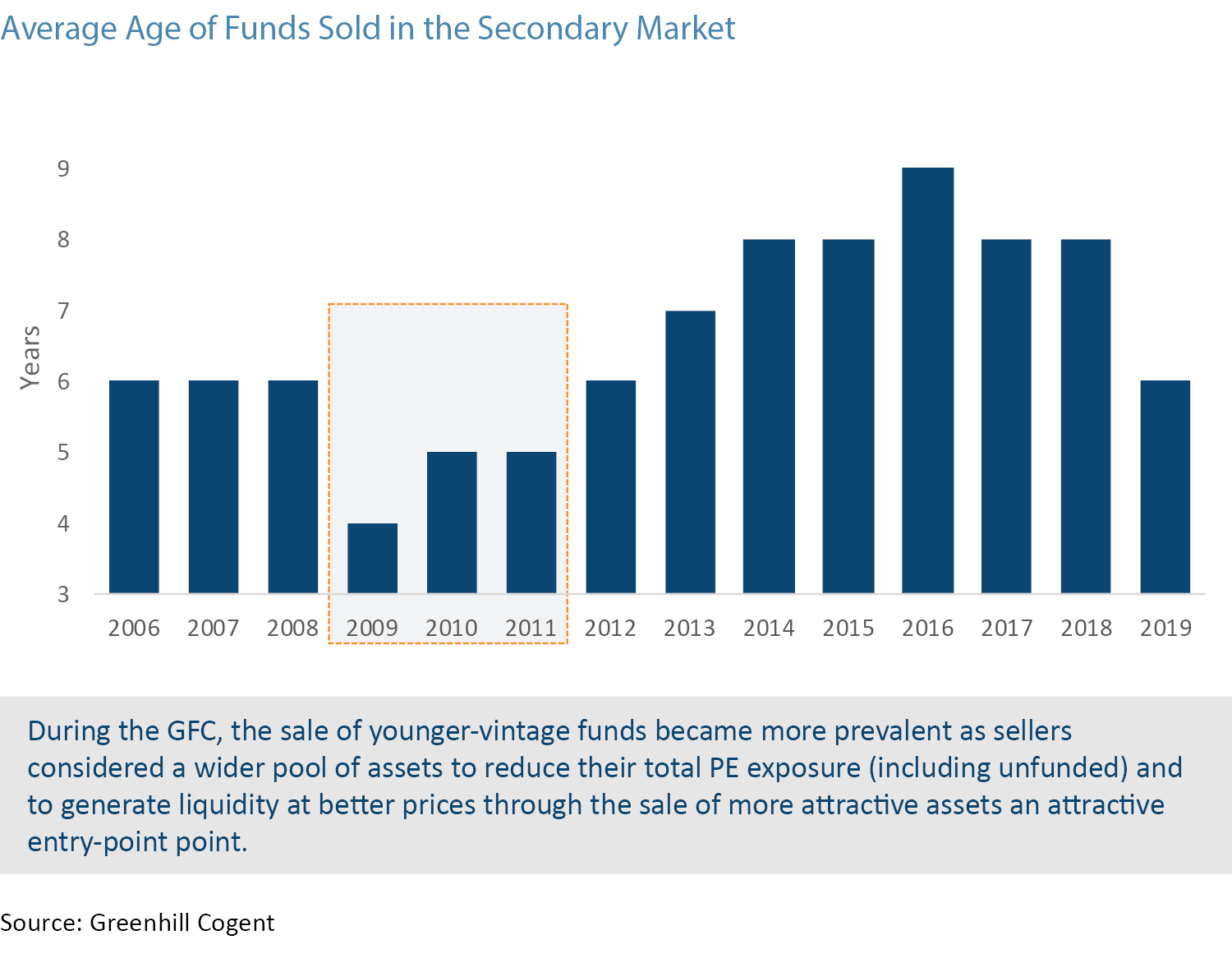

All of the forces described above could create a ‘perfect storm’ and crystallize into specific opportunities – for instance, a limited-time entry point to acquire younger-vintage funds with growth potential. For LPs facing liquidity pressure, the younger-vintage funds are a key stressor, given their significant unfunded capital commitments. At the same time, these assets could be particularly attractive to secondary buyers. Younger-vintage funds have an entry-point advantage in a post-shock world of lower asset valuations, suggesting that buyers could ultimately realize appealing IRRs in the full cycle. But again, such opportunities demand investors with liquidity. Funds with dry powder could be well-positioned to capture such short-term opportunities. Younger vintage funds also potentially offer the secondary buyer with a longer period of time for asset appreciation than tail-end fund interests allowing for higher multiple on invested capita

Increased Structured Solutions Amid Atypical Markets

In this environment, “straight” sales and traditional lending arrangements are prohibitive, both because they depend on transparent valuations and tend to take too long. In contrast, structured solutions can be an appealing substitute. While the cost of capital tends to be marginally higher than a traditional lending solution, there aren’t negative optics for the seller associated with a sale discount, and the speed and flexibility of such arrangements can outweigh the costs. Three examples of these solutions include:

Preferred Equity

Managers. In a preferred equity deal, a GP can accept capital in exchange for preferred equity shares in a diversified fund. The preferred shares are “collateralized” by future distributions from the fund. In a typical arrangement, the fund funnels all or some distributions back to the new preferred shares, paying back the capital infusion plus some pre-determined return – either as a multiple of the investment or as an equivalent IRR. These arrangements can be flexible and allow for the GP to fund portfolio-company balance sheet cures, credit line payoffs, or new acquisitions. Plus, preferred equity solutions may not require LP consent, though we note that it’s still a best practice to make all investors aware of the agreement beforehand, even if formal consent is not required. While some managers may prefer to amend a fund’s recycling provisions to make additional capital available for the remaining portfolio, not every fund will have this as an option.

Institutional investors. The same kind of structured solution is available at the LP level, where the “collateral” is all or part of an LP’s private equity portfolio. Again, this solution provides liquidity to the institution without requiring a headline discount on asset values.

Unfunded Joint Ventures

In some cases, the main demand for capital is to cover unfunded liabilities. For LPs who are comfortable with their existing PE exposure, but would be above their target exposure if there were large capital calls, an unfunded joint venture with a secondary investor would be a way to shift that exposure to a third party. Similar to a preferred equity solution, the secondary investor’s capital injection is repaid with future distributions from the broader portfolio. The terms are customized to each arrangement.

Annex Funds

Managers. In a preferred equity deal, a GP can accept capital in exchange for preferred equity shares in a diversified fund. The preferred shares are “collateralized” by future distributions from the fund. In a typical arrangement, the fund funnels all or some distributions back to the new preferred shares, paying back the capital infusion plus some pre-determined return – either as a multiple of the investment or as an equivalent IRR. These arrangements can be flexible and allow for the GP to fund portfolio-company balance sheet cures, credit line payoffs, or new acquisitions. Plus, preferred equity solutions may not require LP consent, though we note that it’s still a best practice to make all investors aware of the agreement beforehand, even if formal consent is not required. While some managers may prefer to amend a fund’s recycling provisions to make additional capital available for the remaining portfolio, not every fund will have this as an option.

Institutional investors. The same kind of structured solution is available at the LP level, where the “collateral” is all or part of an LP’s private equity portfolio. Again, this solution provides liquidity to the institution without requiring a headline discount on asset values.

Looknig ahead

With a period of restricted volumes, we believe the secondary market could witness a rebound above 2019 levels in 2021-2022, similar to what we saw after the Global Financial Crisis, fueled by an increase in GP-led deals, as exits are pushed further out, and fund lives lapse. We expect the current crisis will result in a return of deeply discounted secondaries. Post GFC discounts averaged 35-40% over 2008-2009 as equities reset, resulting in the highest returns for the cycle.

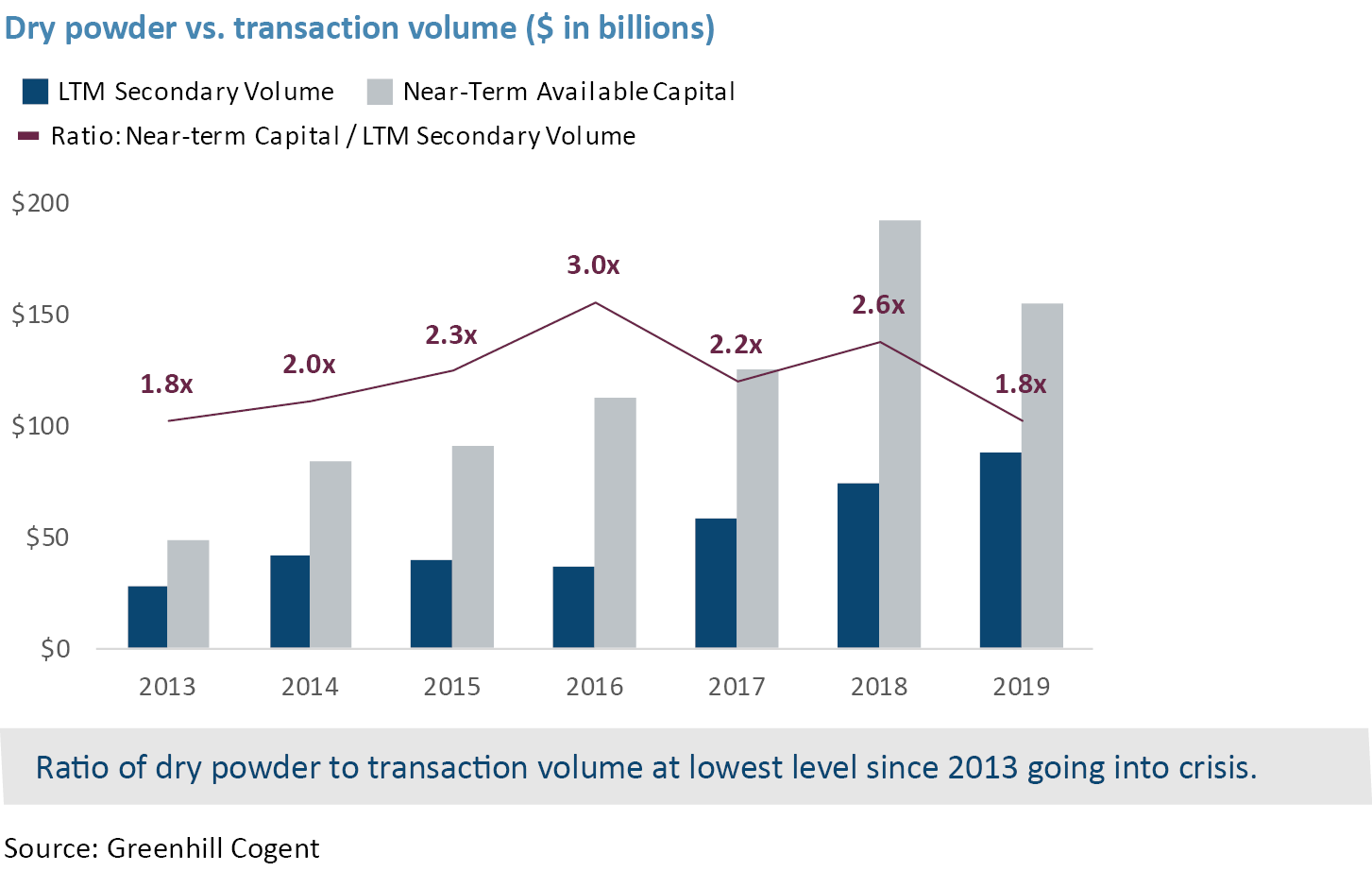

In addition, the dry powder-to-transactions ratio could position buyers even more strongly. Before the pandemic, we saw signs that the market was beginning to favor buyers, as the available dry powder versus annual transaction volume ratio was at its lowest since 2013.

An Environment that Favors Breadth and Depth

The pandemic is driving a new range of market dynamics distinct from other downturns of the modern era. Importantly, the way that managers and investors navigate the present private equity environment will affect their outcomes for years to come.

With a global platform and expertise across a broad range of investing areas, we believe we are one of the strongest secondary solution partners in the industy."

Fred Pollock, Chief Investment Officer, GCM Grosvenor

GCM Grosvenor’s large and unique primary fund portfolio gives us rare visibility into the GP-led market. It also provides a distinctive secondary-sourcing network, useful across all markets but even more powerful in an atypical, liquidity-demanding market. This access to a broad opportunity set is the foundation that allows us to be selective in our deals. Meanwhile, our firm has robust technology resources, enabling our disciplined and systematic approach across opportunities.

The pandemic is providing conditions typical to a traditional recession, but it’s not exactly like any prior event. As such, a unique set of opportunities is available to secondary investors. As some GPs and LPs face liquidity needs, a structured solution that facilitates a quick liquidity transfer could be the key to unlocking these near-term opportunities.

RELATED NEWS AND INSIGHTS

The GP-Led Continuation Vehicle Market: Which Platforms and Strategies are Positioned to Succeed

We explore how long-term relationships and disciplined execution drive differentiated access in middle-market co-investing.

Credit Secondaries: Opportunity, Dispersion, and Discipline

A Q&A with Steve McMillan

Introduction Credit secondaries have emerged as one of the fastest-growing segments of the private markets landscape, driven by a convergence of structural and cyclical forces. Record levels of capital formation,

Important Disclosures

For illustrative and discussion purposes only. The information contained herein is based on information received from third-parties. GCM Grosvenor has not independently verified third-party information and makes no representation or warranty as to its accuracy or completeness. The information and opinions expressed are as of the date set forth therein and may not be updated to reflect new information.

Past performance is not necessarily indicative of future results. No assurance can be given that any investment will achieve its objectives or avoid losses. Investments in alternatives are speculative and involve substantial risk, including strategy risks, manager risks, market risks, and structural/operational risks, and may result in the possible loss of your entire investment. The views expressed are for informational purposes only and are not intended to serve as a forecast, a guarantee of future results, investment recommendations, or an offer to buy or sell securities by GCM Grosvenor. All expressions of opinion are subject to change without notice in reaction to shifting market, economic, or political conditions. The investment strategies mentioned are not personalized to your financial circumstances or investment objectives, and differences in account size, the timing of transactions, and market conditions prevailing at the time of investment may lead to different results. Certain information included herein may have been provided by parties not affiliated with GCM Grosvenor. GCM Grosvenor has not independently verified such information and makes no representation or warranty as to its accuracy or completeness.